What Is Vision Insurance? A Clear Guide to Eye Care Savings

- JF Strawderman

- Apr 20

- 9 min read

TL;DR:

Over 75% of adults need vision correction, but 63% lack vision insurance leading to high out-of-pocket costs.

Vision insurance typically covers exams, eyewear, contacts, and discounts on LASIK, but not medical eye conditions or surgeries.

Using in-network providers, timely scheduling, and understanding benefit cycles maximize savings and health benefits.

Over 75% of adults need some form of vision correction, yet 63% of Americans have no vision insurance at all. That gap is expensive. A single eye exam runs $100 to $200 out of pocket, and a new pair of prescription glasses can easily cost $300 or more without coverage. Vision insurance is often dismissed as a minor add-on, something you tack onto your health plan without thinking much about it. But for millions of families, it is the difference between catching a serious eye condition early and letting it progress undetected. This guide breaks down exactly what vision insurance covers, how the plans work, and who stands to benefit most.

Table of Contents

Key Takeaways

Point | Details |

Covers routine eye care | Vision insurance typically pays for exams, glasses, and contacts, but not major eye surgeries. |

Networks and benefit cycles matter | Staying in-network and using benefits within their valid period maximizes your savings. |

Best for frequent users | Vision insurance saves you most if you or your family need regular eye exams or correction. |

Watch for dual billing | Some procedures trigger both vision and medical insurance, so review your bills and benefits closely. |

What vision insurance covers and how it works

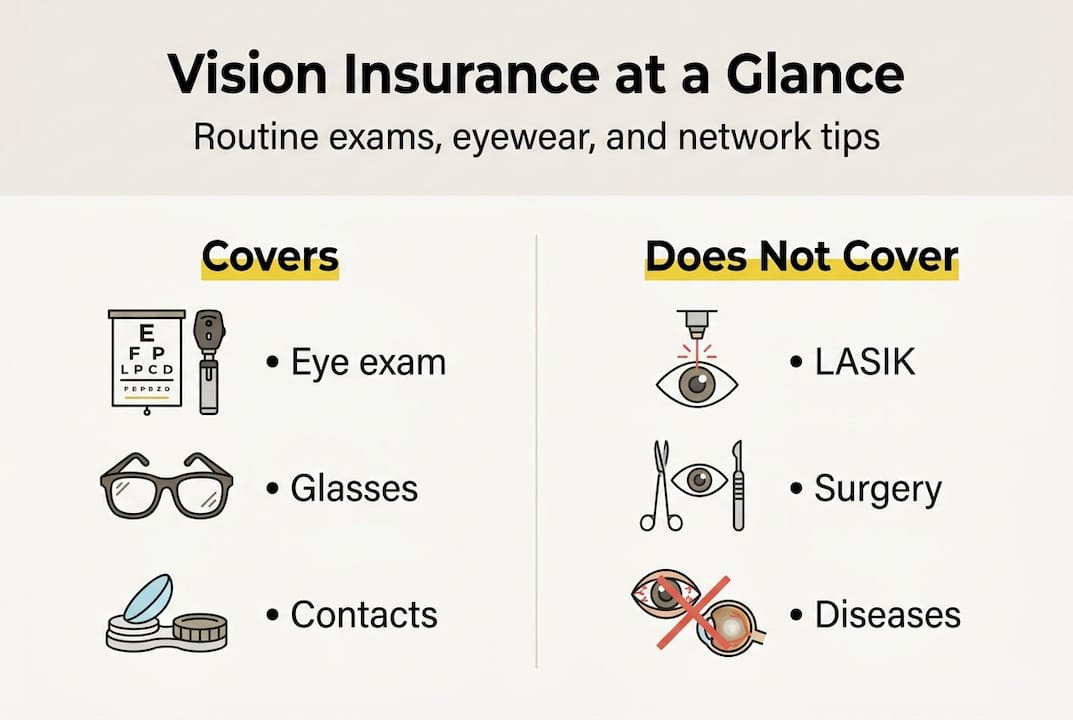

Think of vision insurance as a focused tool, not a catch-all policy. Vision insurance covers routine eye care costs including annual eye exams, prescription eyeglasses, contact lenses, and sometimes discounts on LASIK surgery. It is a supplemental policy, meaning it sits alongside your regular health insurance rather than replacing it. Medical conditions affecting your eyes, such as glaucoma, diabetic retinopathy, or cataracts, are handled by your regular health plan.

Here is what a standard vision insurance policy typically includes:

Annual eye exams with a low copay, usually $10 to $20

Prescription eyeglasses, with a fixed allowance toward frames (commonly $130 to $200) and full or discounted lens coverage

Contact lenses, either as an alternative to glasses or in addition to them, with an annual allowance

LASIK discounts, typically 15% to 20% off at participating providers

Lens enhancements like anti-reflective coatings, sometimes at reduced cost

What vision insurance does not cover is equally important to understand. Surgery for cataracts, treatment for macular degeneration, or managing diabetic eye disease all fall under medical insurance, not vision. Cosmetic procedures are excluded entirely. If you visit an eye doctor for blurry vision caused by diabetes, that visit may be billed under your health plan instead of your vision plan, which is a scenario many people do not expect.

Plans typically operate on annual or 24-month benefit cycles. Your exam benefit may reset every 12 months, while your eyewear allowance resets every 24 months depending on your specific plan. Understanding these cycles matters because unused benefits almost always expire.

Benefit type | Typical coverage | Frequency |

Eye exam | Covered with copay | Every 12 months |

Eyeglass frames | $130 to $200 allowance | Every 12 to 24 months |

Lenses (single vision) | Fully covered | Every 12 months |

Contact lenses | Up to $150 allowance | Every 12 months |

LASIK discount | 15% to 20% off | As eligible |

Pro Tip: Schedule your annual exam and pick up new eyewear near the start of your benefit cycle. This gives you the full benefit window and avoids the scramble of rushing purchases before your plan year ends.

When choosing vision insurance, pay close attention to the allowance amounts for frames and contacts. Plans with lower premiums often come with tighter allowances, which can leave you paying more out of pocket on the back end.

How vision insurance plans work: Networks, benefits, and the fine print

Knowing what is covered is only half the equation. Knowing how to access those benefits without losing money is the other half.

Vision plans operate through provider networks, and staying in-network is critical. Major networks like VSP and EyeMed contract with thousands of eye care professionals nationwide. When you see an in-network provider, you receive the full benefit spelled out in your plan. When you go out of network, the plan may still reimburse you, but at a much lower rate, sometimes as little as $45 for an exam that costs $150. The gap comes out of your pocket.

Benefits reset annually or every 24 months, and unused benefits almost never roll over. If you skip your annual exam in November, you do not get two exams in January. That benefit is simply gone.

Common pitfalls that cost people money include:

Missing the benefit window by waiting too long to schedule an exam or order eyewear

Assuming all eye doctors accept your plan without verifying network status first

Confusing your exam benefit with your eyewear benefit, since they may reset on different schedules

Buying frames that exceed your allowance without knowing the out-of-pocket cost beforehand

Not using secondary riders that some plans include for additional lens upgrades

Understanding health insurance types explained helps clarify where vision fits within the broader coverage picture, especially when coordinating benefits across multiple policies.

Feature | Group vision plan | Individual vision plan |

Access | Through employer | Purchased directly |

Cost | Usually lower (employer contributes) | Higher premium, no employer subsidy |

Flexibility | Limited to employer’s options | Choose your own plan and network |

Best for | Employees with employer benefits | Self-employed, freelancers, retirees |

For families weighing group vs individual vision plans, the decision often comes down to how much flexibility you need and whether your preferred eye doctor participates in the employer’s network.

Pro Tip: Set a calendar reminder two to three months before your benefit year ends. This gives you enough time to schedule an exam, choose frames, and complete your order before unused benefits disappear.

When choosing a plan, always confirm that your current eye doctor is in-network before you enroll. Switching providers just to stay in-network is a frustrating surprise that catches many families off guard.

Who benefits most from vision insurance (and when it’s not worth it)

Not everyone gets the same return from vision insurance. The value depends almost entirely on how much eye care you actually use.

Here is the telling reality: insured patients are twice as likely to get annual exams, and eyewear purchase rates are 66% among insured patients compared to 54% for those paying out of pocket. When 75% of adults need some form of vision correction, that gap in access is a real health issue, not just a financial one.

According to Forbes Advisor, vision insurance delivers genuine savings for glasses and contacts users, families, and those who rely on frequent exams, often saving hundreds of dollars per year. Early detection of conditions like high blood pressure, diabetes, and even certain cancers can happen during a routine eye exam, making the value extend well beyond just eyewear costs.

Who benefits most from vision insurance:

Glasses or contact lens wearers who buy new prescriptions annually

Families with children, who often need more frequent prescription updates

Adults over 40, where the risk of age-related eye conditions rises

People with diabetes or a family history of eye disease

Anyone whose employer offers group vision coverage at low or no cost

Who might consider skipping or using a discount plan instead:

People with consistently perfect vision who visit an eye doctor less than once every few years

Individuals who already receive free or heavily subsidized eye care through another program

Those whose preferred providers are not in any available network

The math is straightforward. If you pay $15 per month for vision coverage and use your exam and eyewear benefits each year, you are likely saving money compared to paying out of pocket. Consult a step-by-step coverage guide to run the actual numbers for your situation before deciding.

Special cases: Dual billing, LASIK, and maximizing your coverage

Beyond the basics, a few specific scenarios trip up even the most prepared insurance shoppers.

Dual billing happens when an eye exam qualifies under both your vision plan and your medical insurance. If your doctor checks for signs of diabetic retinopathy during your routine exam, that portion may be billed to your health plan. Nearly 43% of patients are surprised when they receive two separate bills after a single eye appointment. Knowing this in advance prevents confusion and helps you plan for potential out-of-pocket costs.

LASIK coverage is a common misunderstanding. Vision insurance does not pay for LASIK outright. It provides discounts, typically 15% to 20% off at participating providers. Post-LASIK, your eligibility for contact lens benefits often changes because the procedure is considered corrective, meaning contact lenses are no longer deemed medically necessary under many plan definitions. Understanding insurance terms explained helps you read the fine print before committing to a procedure.

If you have two vision insurance plans, coordination rules apply. You can use both, but using two vision plans requires careful billing. One plan is designated primary and the other secondary. The combined benefit cannot exceed your actual cost, which is called the no-duplication rule.

Three tips for getting maximum value from your vision benefits each year:

Plan your exam and eyewear purchase in the same visit cycle so both benefits are used before the window closes.

Confirm network participation for every provider before scheduling, not after.

Buy within your benefit window and avoid holding off on eyewear orders past the plan year end date.

“Almost half of consumers are caught off guard by receiving separate bills from the same eye appointment. Knowing how dual billing works before your visit saves time, stress, and money.”

The real value of vision insurance: Beyond the numbers

Most articles about vision insurance stop at the math. Premium versus out-of-pocket cost, eyewear allowances, and whether you break even. But that framing misses something important.

Regular eye exams detect more than refractive errors. Optometrists routinely identify early signs of high blood pressure, diabetes, multiple sclerosis, and even certain tumors during a standard exam. For families, especially those with young children or aging parents, vision insurance is a reason to show up for those exams consistently, even when everything feels fine.

There is also a behavioral angle that rarely gets discussed. People with vision insurance are simply more likely to use eye care services. That increased usage translates to earlier detection, fewer surprises, and better long-term health outcomes. Dismissing vision insurance as a bad deal in years when you do not buy new glasses is like dismissing smoke detectors because your house did not catch fire.

For clients managing pre-existing conditions and coverage, vision insurance can be one layer of a broader prevention strategy that pays off in ways that never show up on a premium comparison spreadsheet.

Pro Tip: Use your covered annual exam even in years you do not need new glasses. The exam itself has value as a health screening, not just a prescription update.

Get help with your vision, health, and financial protection

Figuring out the right vision plan alongside your health, life, and retirement coverage can feel like a lot to sort through on your own. Allowances, network rules, benefit cycles, and dual billing all add complexity that is easy to get wrong without guidance.

At Strawderman Financial, we help families and individuals navigate exactly these decisions. Whether you are evaluating health insurance options alongside vision coverage or looking at how life insurance plans fit into your broader financial picture, our agents provide personalized guidance with no pressure and no jargon. Schedule a free consultation and find out how the right coverage combination can protect your health and your budget at the same time.

Frequently asked questions

Does vision insurance cover eye surgery like LASIK or cataracts?

Vision insurance typically offers discounts, not full coverage, on LASIK, while cataract surgery is considered a medical procedure covered under your regular health insurance plan.

What’s the difference between vision and health insurance?

Vision insurance covers routine care like exams and glasses, while health insurance covers eye diseases, injuries, and surgical procedures such as cataract removal or treatment for glaucoma.

How often can I use my vision insurance benefits?

Most plans cover one exam per year and new glasses or contacts every 12 to 24 months, with unused benefits typically expiring at the end of the plan year.

What happens if I have two vision insurance plans?

You can coordinate dual vision plan benefits with one plan acting as primary and the other as secondary, but combined reimbursements cannot exceed your actual cost under the no-duplication rule.

Recommended

Comments