How to evaluate dental insurance: smart steps for best coverage

- JF Strawderman

- Apr 27

- 9 min read

TL;DR:

Many people choose dental plans based solely on premiums without understanding coverage limits and exclusions.

Calculating total yearly costs by adding premiums, deductibles, coinsurance, and hidden fees ensures better plan comparison.

Verifying dentist network status and considering insurer reputation are key to avoiding unexpected out-of-pocket expenses.

You finally use your dental insurance for a crown, only to discover your plan maxes out at $1,000 and you still owe $800 out of pocket. That frustration is more common than you’d think, and it almost always comes down to one thing: people choose dental insurance based on the monthly premium alone without reading the fine print. This guide walks you through every step you need to take to compare plans clearly, spot the hidden costs before they hit you, and find coverage that actually fits your family’s real dental needs.

Table of Contents

Key Takeaways

Point | Details |

Check annual maximums | Most dental plans have an annual limit on coverage that rarely gets reached but impacts big expenses. |

Calculate true costs | Factor in premiums, deductibles, co-pays, and possible exclusions to avoid billing surprises. |

Verify in-network coverage | Your out-of-pocket costs are often lower if you use dentists that are in your plan’s network. |

Review ratings and feedback | Plan quality, customer service, and satisfaction can vary—compare reviews before you buy. |

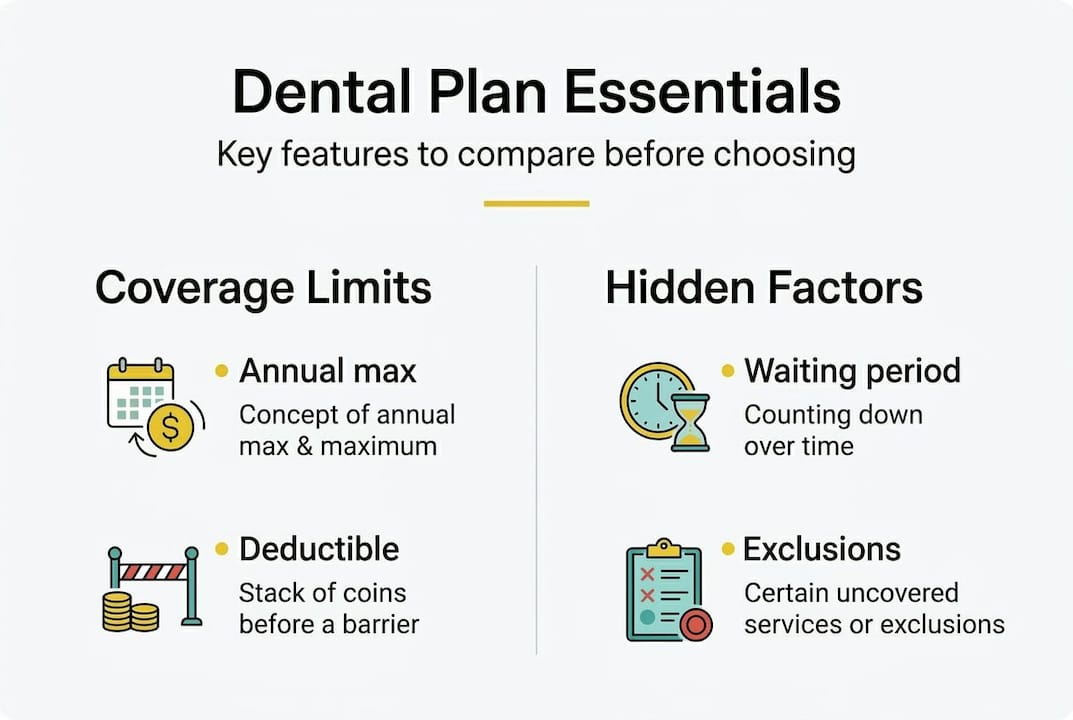

Know what to look for: Essential dental insurance features

Once you understand why evaluating dental insurance matters, the first step is identifying the features that should always be on your radar. Not all dental plans are built the same, and the differences between them can mean hundreds or even thousands of dollars each year.

Annual maximums are one of the most important numbers in any dental plan. This is the highest dollar amount your insurer will pay for covered services within a single plan year. According to annual maximums data, annual maximums typically fall between $1,000 and $2,000 per person, and only about 3 to 7 percent of patients actually reach that limit in any given year. That sounds reassuring until you need a root canal, a crown, and a filling in the same calendar year.

Deductibles are what you pay before your insurance kicks in. Individual deductibles usually range from $50 to $150 per year. Family plans are trickier. Some use an individual deductible model where each family member has their own threshold. Others use an aggregate deductible, meaning the whole family shares one combined limit. Understanding dental insurance coverage basics helps you figure out which structure works better for your household size and dental history.

Waiting periods are another feature that catches people off guard. Many plans require you to wait 6 to 12 months before they’ll cover major services like crowns, bridges, or dentures. If you need significant dental work soon, a plan with a long waiting period could leave you paying full price anyway.

Here’s a quick look at how common plan features compare:

Feature | Basic plans | Mid-tier plans | Premium plans |

Annual maximum | $1,000 | $1,500 | $2,000+ |

Individual deductible | $100-$150 | $50-$100 | $0-$50 |

Waiting period (major) | 12 months | 6 months | None or minimal |

Preventive coverage | 100% | 100% | 100% |

Major services covered | 50% | 60-70% | 80% |

Common exclusions to watch for include:

Cosmetic procedures like whitening or veneers

Orthodontics (often a separate rider)

Pre-existing conditions in some plans

Implants (excluded by many standard plans)

Services received out-of-network at higher cost

Pro Tip: Always read the “exclusions and limitations” section of any plan before you sign up. It’s usually buried at the back of the benefits document, but it tells you exactly what the plan won’t pay for.

Calculate the true cost: Premiums, out-of-pocket, and hidden fees

After you know what to look for in a plan, it’s time to demystify what you’ll actually pay each year. The monthly premium is just the starting point. The real cost of dental insurance includes your deductible, copays, coinsurance, and anything the plan simply doesn’t cover.

The key principle here is to calculate total cost by adding your premium plus out-of-pocket expenses, not just the premium alone. A plan with a $20 monthly premium sounds attractive, but if it only covers 50 percent of basic services after a $150 deductible, you could end up paying far more than a $45 per month plan with stronger coverage.

Here’s a sample annual cost breakdown for a family of four with moderate dental needs:

Cost category | Low-premium plan | Mid-tier plan |

Annual premium | $480 | $1,080 |

Deductibles (family) | $400 | $200 |

Coinsurance (fillings, etc.) | $350 | $200 |

Services not covered | $300 | $100 |

Total estimated cost | $1,530 | $1,580 |

In this scenario, the “cheap” plan and the mid-tier plan cost nearly the same total amount. But the mid-tier plan offers better coverage, less stress, and fewer surprise bills. Understanding health insurance cost factors applies directly to dental plans too since the same logic of balancing premiums against out-of-pocket risk holds true.

Follow these steps to calculate your true annual dental insurance cost:

Multiply the monthly premium by 12 to get your annual premium.

Add your expected deductible based on your family’s dental history.

Estimate coinsurance costs for services you typically use each year.

Add any costs for services your plan excludes that you’ll need anyway.

Compare that total across at least three different plan options.

For major procedures like implants, even a strong dental plan may not cover the full cost. Exploring financing dental treatments can help you plan for procedures that exceed your annual maximum, so you’re never caught flat-footed.

Pro Tip: Keep a simple spreadsheet with each plan’s true annual cost estimate. It takes 20 minutes and could save your family hundreds of dollars every year.

Check provider networks, reviews, and plan reliability

Knowing the numbers is just one side. The experience and reliability of coverage make a big difference too. A plan that looks great on paper can still disappoint if your preferred dentist isn’t in-network or if the insurer is slow to process claims.

Provider networks directly affect both your access to care and your out-of-pocket costs. When you see an in-network dentist, the insurer has negotiated discounted rates, so your coinsurance applies to a lower base cost. When you go out-of-network, you often pay the difference between what the dentist charges and what the insurer considers “usual and customary.” That gap can be significant, sometimes hundreds of dollars per visit.

To verify your dentist is in-network, use these steps:

Visit the insurer’s website and search their provider directory.

Call your dentist’s office directly and ask which insurance plans they accept.

Confirm the specific plan name, not just the insurance company, since some insurers offer multiple network tiers.

Re-verify annually, because network participation changes.

Third-party ratings add another layer of confidence. Checking ratings from sources like J.D. Power and AM Best gives you an objective view of insurer reliability and customer satisfaction. J.D. Power scores reflect how policyholders feel about claims handling and communication. AM Best ratings assess the insurer’s financial strength, which matters if you ever need to file a large claim.

“The best dental plan is one your dentist accepts, your family will actually use, and that won’t surprise you with a bill you didn’t see coming.”

User reviews on platforms like Google, Trustpilot, and state insurance department complaint databases reveal patterns that ratings alone don’t capture. Watch for recurring complaints about claim denials, slow reimbursements, or confusing billing. A few negative reviews are normal, but a pattern of the same complaint is a red flag. Research on insurance and patient satisfaction shows that trust in your provider directly affects whether patients follow through with recommended care.

Understanding the difference between group versus individual dental plans also matters here. Group plans through an employer often have pre-negotiated networks and lower premiums, but individual plans give you more control over which network and insurer you choose.

Compare plans side-by-side for your specific needs

With all the groundwork covered, you’re ready to put potential plans side-by-side and make a truly informed choice. Comparing plans without a clear framework leads to decision fatigue and usually results in picking the wrong plan for the wrong reasons.

Start by setting your priorities. Ask yourself: Is keeping my current dentist the top priority? Is minimizing monthly cost most important? Does my family have upcoming major dental work that needs strong coverage now? Your answers should drive every trade-off you make.

As noted by dental quality comparison research, the quality of care you receive is often tied to how well your insurance aligns with your specific treatment needs, not just the plan’s overall rating.

Here’s a side-by-side comparison framework:

Criteria | Plan A | Plan B | Plan C |

Monthly premium | $25 | $45 | $60 |

Annual maximum | $1,000 | $1,500 | $2,000 |

Waiting period (major) | 12 months | 6 months | None |

My dentist in-network? | No | Yes | Yes |

Preventive coverage | 100% | 100% | 100% |

Major services | 50% | 70% | 80% |

Orthodontic coverage | No | No | Yes (rider) |

It’s also worth noting that family plans may have individual or aggregate deductibles, which changes how quickly your coverage kicks in for each family member. An aggregate deductible means one sick family member can use up the family’s entire deductible, leaving less buffer for others.

Follow this repeatable process each enrollment period:

List your must-haves: in-network dentist, no waiting period, orthodontic coverage.

List your nice-to-haves: low deductible, high annual maximum, strong insurer ratings.

Pull at least three plan options and fill in the comparison table above.

Calculate the true annual cost for each plan using the method from Section 2.

Eliminate any plan that fails a must-have requirement.

Choose the plan with the best true cost and coverage fit from what remains.

Understanding health insurance plan types can also sharpen your comparison skills, since dental plans often mirror the same HMO, PPO, and indemnity structures used in medical insurance. A dental HMO typically costs less but restricts you to a specific network. A dental PPO costs more but gives you flexibility to see any licensed dentist.

The hidden pitfalls most people miss when evaluating dental insurance

Even after a careful comparison, there are pitfalls that catch many smart shoppers off guard. We’ve seen this pattern repeat itself, and it’s worth calling out directly.

The biggest misconception is about annual maximums. Most people assume they’ll hit their $1,500 limit every year and plan accordingly. In reality, only a small fraction of policyholders ever reach their annual maximum. The danger runs in the opposite direction: people overvalue high annual maximums and overpay in premiums for coverage they’ll never use. If your family’s dental history is routine checkups and the occasional filling, a plan with a $1,000 maximum and a lower premium may serve you better than a $2,000 maximum plan with a much higher monthly cost.

The second pitfall is premium fixation. Choosing the lowest premium feels financially responsible, but it often backfires. A low-premium plan with a 12-month waiting period on major services is essentially useless if you need a crown in month three. You’ll pay out of pocket anyway, plus the monthly premium. That’s the worst of both worlds.

The third pitfall is ignoring personal dental history. A plan that’s rated number one by a consumer publication may be a poor fit for your family’s specific needs. If you have teenagers who need orthodontic work, a plan without orthodontic coverage is a bad deal regardless of how well it scores overall. Protecting your health and finances means choosing coverage that matches your actual risk profile, not someone else’s average.

Finally, don’t overlook the insurer’s claims process. A plan can have excellent benefits on paper but a frustrating, slow claims experience in practice. That experience affects whether you actually use your coverage or avoid the dentist to sidestep the hassle.

Get expert help to choose the best dental insurance for you

Choosing the right dental plan takes real effort, and even careful shoppers sometimes miss details that cost them later. That’s where working with a knowledgeable insurance advisor makes a genuine difference.

At Strawderman Financial, we work with individuals and families across the United States to find dental and vision coverage that fits their real lives, not just a generic average. Our agents take the time to understand your dental history, your budget, and your preferred providers before recommending a plan. We also help clients look at the bigger picture, connecting dental coverage with life insurance planning and retirement planning services so your financial protection is truly complete. Schedule a free consultation and let us do the heavy lifting for you.

Frequently asked questions

What is an annual maximum in dental insurance?

An annual maximum is the highest amount your dental plan will pay for covered services in a plan year, usually $1,000 to $2,000 per person, after which you pay 100 percent of any additional costs.

How do I know if my dentist is in-network?

Verify your dentist’s status by searching your insurer’s online provider directory or calling your dentist’s office directly to confirm which specific plans they accept.

Are premiums the only cost for dental insurance?

No. Beyond your monthly premium, you’ll also pay deductibles, copays, coinsurance, and the full cost of any services your plan excludes. Always calculate total cost including all out-of-pocket expenses before choosing a plan.

What’s the difference between individual and family dental plans?

Family plans may use individual or aggregate deductibles, and annual maximums may apply per person or across the family, which significantly changes how much coverage each member actually receives.

Why do plan ratings and reviews matter?

Ratings from J.D. Power and AM Best signal insurer reliability and financial strength, while user reviews reveal real-world claims experiences that official ratings don’t always capture.

Recommended

Comments