Vision Insurance Explained: How It Protects Your Health and Wallet

- JF Strawderman

- Apr 29

- 10 min read

TL;DR:

Vision insurance covers preventive eye exams, glasses, and contact lenses, not eye surgeries or medical conditions.

Costs for plans vary from $5 to $50 monthly in 2026, influenced by coverage type and provider networks.

It is valuable for early detection of systemic health issues and benefits those with vision correction needs.

Most people assume vision insurance is only useful if they already wear glasses or contacts. That assumption costs Americans real money every year. Vision insurance is supplemental coverage designed for routine preventive eye care, including annual exams, prescription eyewear, and frames, but it offers far more than just help buying a new pair of lenses. This guide breaks down exactly what vision coverage provides, how much it costs in 2026, who benefits most, and how to pick the right plan for your family’s health and financial security.

Table of Contents

Key Takeaways

Point | Details |

Covers routine eye care | Vision insurance pays for eye exams, glasses, and contacts but not medical eye conditions. |

2026 premium changes | Costs are rising this year due to healthcare inflation and new eyewear technology. |

Value goes beyond glasses | Annual vision exams catch serious health issues early, making coverage worthwhile for many people. |

Best value in employer plans | Employer-sponsored vision insurance typically offers the lowest premiums and best benefits. |

Pair with financial planning | Vision insurance can strengthen overall financial security when integrated with health and life coverage. |

What does vision insurance really cover?

Let’s clear up the confusion right away. Vision insurance and standard health insurance are not the same thing, and they do not overlap in the way most people expect. Understanding that difference saves you from being caught off guard when a bill arrives.

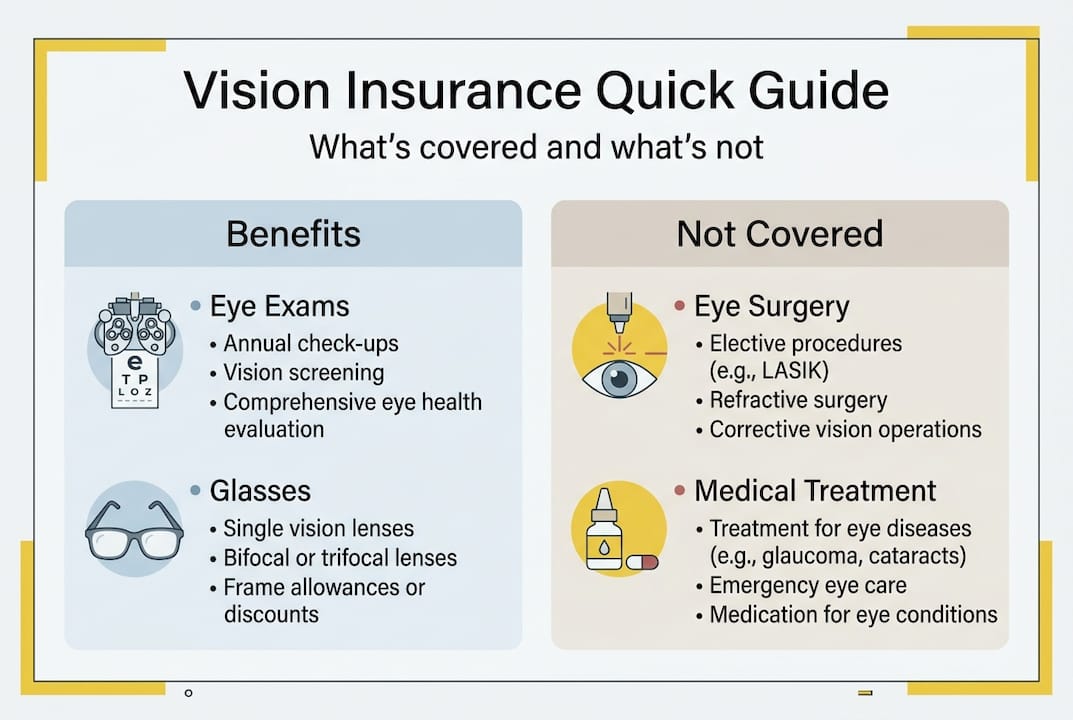

What vision insurance typically covers:

Annual comprehensive eye exams

Prescription eyeglasses (frames and lenses)

Basic contact lens fittings and supplies

Lens upgrades such as anti-reflective coating or progressive lenses (often at a discounted rate)

Discounts on additional pairs of glasses

Most plans follow one of two structures. The first is a vision benefits plan, which works like traditional insurance with copays and allowances. You pay a monthly premium and then pay a fixed copay at each visit. The second is a discount vision plan, which gives you reduced rates at participating providers without the monthly premium structure of a true insurance product.

What vision insurance does NOT typically cover:

Covered | Not Covered |

Annual eye exams | Eye surgery (LASIK, cataract removal) |

Prescription glasses | Treatment for glaucoma or macular degeneration |

Contact lens fitting | Infections or eye injuries |

Frame allowances | Refractive surgery complications |

Lens coatings (partial or discounted) | Medical diagnosis of retinal conditions |

Medical eye conditions fall under your standard health insurance policy, not vision insurance. That is a critical distinction. If you develop glaucoma, an eye infection, or need surgery, your regular health plan handles those costs.

Here is something that surprises many people: vision insurance is genuinely valuable even if you have perfect eyesight and never plan to buy glasses. Annual eye exams are about far more than getting a prescription. A trained optometrist can detect early signs of diabetes, high blood pressure, multiple sclerosis, and even certain cancers during a routine exam. Skipping that exam means skipping a powerful early-warning system for your overall health.

“Routine eye exams are one of the most underused preventive health tools available to Americans. Many systemic diseases show early signs in the eyes before symptoms appear anywhere else in the body.”

You can explore more cost-saving strategies in our vision insurance savings guide, which walks through how to get the most value from your plan from day one.

What to expect from most vision insurance plans:

One covered eye exam per year with a small copay (typically $10 to $25)

A frame allowance between $100 and $200 toward new glasses

A contact lens allowance that varies by plan and brand

Discounts of 20 to 40 percent on lens upgrades not fully covered

Access to in-network optometrists and optical retailers

The key is reading the fine print. Some plans limit which frames qualify for the full allowance, and some have waiting periods before benefits kick in. Knowing the details of your specific plan prevents unwanted surprises at the register.

How much does vision insurance cost in 2026?

Understanding cost is where many families get stuck. Vision insurance premiums are not one-size-fits-all, and 2026 brings some notable changes worth knowing before you budget.

Individual plans range from $5 to $38 per month, while family plans typically run $25 to $50 per month. Employer-sponsored vision coverage is almost always the most affordable option because your employer covers a portion of the premium. When you purchase coverage on your own, called a standalone or individual market plan, you pay the full cost yourself.

Comparison of plan types in 2026:

Plan Type | Monthly Cost (Individual) | Monthly Cost (Family) | Enrollment Period |

Employer-sponsored | $5 to $15 (employee share) | $10 to $25 (employee share) | Open enrollment only |

Standalone insurance plan | $15 to $38 | $30 to $50 | Anytime |

Discount vision plan | $8 to $20 | $15 to $30 | Anytime |

So why are premiums climbing in 2026? Several forces are pushing costs upward at the same time. Advanced lens technology, including digital lenses and blue-light-blocking coatings, has become standard for many patients and drives up manufacturing costs. Healthcare inflation continues to affect every corner of the industry, including optometry. Supply chain disruptions affecting optical components, frame materials, and contact lens raw materials have not fully resolved since prior years, and those added costs get passed to consumers and insurers alike.

Factors that influence your vision insurance cost:

Your age and the ages of family members on the plan

Whether you access in-network or out-of-network providers

The eyewear frame and lens allowance your plan provides

Geographic location, since optometry costs vary significantly by region

The specific benefits tier you select (basic vs. enhanced plans)

You can track how these vision insurance trends are evolving as the year progresses, since premium structures may adjust mid-year for some carriers.

Here is a number that puts all of this in perspective. Vision disorders cost the U.S. economy an estimated $199.6 billion per year in lost productivity, treatment, and caregiver time. When you factor in that number, the cost of a monthly premium looks far smaller relative to the economic burden of unaddressed vision problems.

For families deciding between a health plan upgrade or adding vision coverage separately, it helps to understand health insurance types explained at a broader level, since the interaction between your medical and vision benefits affects your total out-of-pocket spending. Additionally, if you have a history of health complications, understanding the role of pre-existing conditions can clarify how those factors interact with supplemental plans like vision insurance.

Who really needs vision insurance—and who doesn’t?

This is the question everyone is actually asking. The answer is more nuanced than “everyone should have it” or “skip it if you have good eyes.”

63% of Americans lack vision insurance, and 40% of adults have not had an eye exam in the past year. That is a significant portion of the population flying blind on their eye health, literally and financially. Employees who have vision coverage through work are twice as likely to get their annual eye exam compared to those without coverage. Given that 75% of adults need some form of vision correction, the math is fairly clear about who benefits.

Ask yourself these questions to decide if vision insurance makes sense for you:

Do you or anyone in your family wear glasses or contact lenses?

Have you or a family member been told you are at risk for eye disease?

Do you have a family history of diabetes, high blood pressure, or glaucoma?

Are you over 40, when the risk of vision changes increases significantly?

Do you have children who have not had a recent eye exam?

Would an unexpected $300 to $600 eyewear or exam bill create financial stress?

Does your employer offer vision coverage at little or no additional cost?

If you answered yes to even two or three of those questions, vision insurance is likely worth it for your situation.

Who benefits most:

Children benefit enormously from vision coverage. Uncorrected vision problems are one of the most common undiagnosed issues affecting school-age kids, and the effects on learning and development can be serious. Older adults face increasing risks of cataracts, macular degeneration, and glaucoma. And individuals with a personal or family history of diabetes should prioritize eye exams, since diabetic retinopathy is a leading cause of adult blindness.

Pro Tip: To quickly estimate whether vision insurance will save you money, add up your expected annual eye care costs without insurance. A single comprehensive exam costs $100 to $200 out of pocket. New glasses can run $200 to $600. New contact lenses for a year might cost $300 to $600. If your total likely exceeds what you would pay in annual premiums plus copays, vision insurance puts money back in your pocket.

For families weighing individual versus group plan options, reviewing the difference between group vs individual health plans can help frame that decision more clearly across all your insurance needs.

How to choose the right vision insurance plan

Now that you know what vision insurance covers, what it costs, and whether you need it, the final step is selecting the right plan with confidence. This part does not need to be complicated if you follow a clear process.

Start with your employer. If your workplace offers vision coverage, that is almost always your best option. Employer-sponsored plans are typically the most cost-effective choice because your employer absorbs part of the premium cost, and the group purchasing power keeps coverage richer than what you might find on the individual market. If your employer does not offer vision coverage, standalone plans available through insurance carriers or associations allow you to enroll at any time during the year.

What to compare when shopping for a vision plan:

Monthly premium versus your estimated annual out-of-pocket costs without coverage

Copay amounts for exams, frames, and contact lenses

Frame and lens allowance limits and whether your preferred brands fall within network

Provider network size and whether your current optometrist participates

Lens upgrade discounts for coatings, transitions, or premium lens types

Contact lens benefits if you wear contacts rather than glasses

Waiting periods before specific benefits become active

One mistake many people make is choosing a plan based purely on the lowest premium without checking the network. A slightly higher premium with a broader network often saves more money in practice because you are not forced to switch doctors or pay out-of-network rates.

Pro Tip: Pair your vision plan with a Flexible Spending Account (FSA) or Health Savings Account (HSA) if you have access to either. Both accounts allow you to use pre-tax dollars for qualifying vision expenses including exams, glasses, contact lenses, and prescribed eye drops. Using an FSA or HSA alongside vision insurance effectively gives you a discount equal to your marginal tax rate on top of your plan benefits.

For a deeper walkthrough of the selection process, our guide on choosing vision insurance walks through every decision point in plain language. And if you are also reviewing your broader health coverage, our guide on health insurance selection tips is a natural companion resource for 2026 planning.

A perspective most people miss: Vision insurance is about prevention, not just eyewear

Here is something the standard vision insurance conversation almost never addresses. When most people calculate whether vision insurance is worth it, they only count the glasses or the exam copay. They are missing the bigger picture entirely.

An annual eye exam is one of the few preventive health touchpoints that can catch serious systemic disease before you have any symptoms. High blood pressure, diabetes, autoimmune disorders, and even certain brain conditions can leave traces visible to a trained optometrist during a routine exam. That early detection is not just a health benefit. It is a financial one. Catching a condition early almost always costs far less to treat than discovering it late.

We have seen too many people choose discount vision plans or skip coverage altogether to save a few dollars a month, only to face significant out-of-pocket costs when a problem emerges that could have been caught earlier. Discount plans look attractive on the surface, but for anyone who sees a doctor regularly or wears corrective lenses, they rarely match the actual value of a true insurance plan.

Vision insurance, viewed through this broader lens, is not a luxury add-on. It is a smart layer in a complete financial and health protection strategy. Our broader vision insurance value resource expands on exactly this idea if you want to explore further.

Explore vision protection and financial wellness together

Vision insurance is one piece of a larger picture. At Strawderman Financial, we help individuals and families across the U.S. understand how every layer of their coverage, from vision and dental to life insurance and retirement savings, fits together into a plan that actually protects them.

If you are exploring vision insurance options or doing a full review of your family’s health and financial coverage in 2026, our agents are ready to walk through your situation at no cost. We connect the dots between your life insurance solutions and your financial planning services so that nothing falls through the cracks. Schedule your free consultation today and get a clear, complete view of your protection plan.

Frequently asked questions

Does vision insurance cover eye surgery, like LASIK or cataract removal?

No, routine vision insurance does not cover eye surgeries or medical eye conditions. These are handled by health insurance, not a supplemental vision plan.

Can I enroll in vision insurance at any time in 2026?

Standalone vision insurance plans generally allow enrollment at any time, while employer-sponsored vision plans typically restrict sign-ups to your company’s open enrollment period.

Is vision insurance worth it if I only need a checkup once a year?

Yes, even for people without glasses, vision insurance can be worthwhile because annual exams detect early signs of systemic health issues like diabetes and high blood pressure before symptoms develop.

How do I decide between an employer plan and a standalone vision plan in 2026?

Compare total costs, including premiums, copays, and network access. Employer-sponsored plans are typically less expensive, but standalone plans offer enrollment flexibility and may suit self-employed individuals or those between jobs.

Recommended

Comments