What is life insurance? Protect your family's future

- JF Strawderman

- Apr 30

- 10 min read

TL;DR:

Life insurance is a vital financial tool that protects families from income loss and debts.

Term life offers affordable, temporary coverage, while whole life provides lifelong protection with cash value.

Choosing the right policy and honestly applying ensures your family receives benefits when needed.

Most people assume life insurance is something you buy when you’re retired, wealthy, or expecting the worst. That assumption costs families dearly. Life insurance is one of the most practical financial tools available to everyday Americans, regardless of age or income. It protects the people who depend on you, covers the debts that don’t disappear when you do, and gives your family breathing room during one of the hardest times imaginable. This article breaks down what life insurance is, how it works, the main types, how payouts happen, and how to choose the right coverage for your family.

Table of Contents

Key Takeaways

Point | Details |

Life insurance basics | It is a contract that pays your loved ones a set benefit if you die during coverage. |

Main policy types | Term life is simple and affordable for most, while whole life includes cash value but is more expensive. |

Payout process | Beneficiaries usually get a tax-free lump sum in 14-60 days after filing a claim. |

Choosing coverage | Select a policy by matching your family’s needs, being honest on the application, and reviewing terms closely. |

Expert advice matters | Speaking with a licensed advisor helps you avoid mistakes and get the best value. |

Defining life insurance and its core components

Life insurance is a legal contract between you and an insurance company. You agree to pay regular premiums, and the insurer agrees to pay a set amount of money to your chosen beneficiaries when you die. Simple concept, enormous impact.

Understanding why buy life insurance matters starts with knowing what a policy actually contains. Every life insurance policy has a few essential parts:

Premium: The amount you pay regularly, usually monthly or annually, to keep the policy active.

Death benefit: The lump sum the insurer pays to your beneficiaries when you pass away while covered.

Beneficiaries: The people or organizations you name to receive the death benefit.

Policy term or permanence: Whether coverage lasts a set number of years or your entire life.

Cash value: A savings component available in some permanent policies that grows over time.

Riders: Optional add-ons that customize your coverage, such as critical illness coverage or accidental death benefits.

As key components include premium payments, death benefit, beneficiaries, policy term or permanence, and optional cash value or riders, each element plays a direct role in how your policy functions and what your family receives.

Families use life insurance for a wide range of financial reasons. The most common are replacing a lost income stream when a breadwinner dies, paying off a mortgage or other debts, covering funeral and burial costs, funding a child’s education, and simply providing financial security during a chaotic time.

“Life insurance isn’t about dying. It’s about making sure the people you love can keep living their lives without financial collapse.”

Pro Tip: When choosing your beneficiaries, name both a primary beneficiary and a contingent beneficiary. The contingent beneficiary receives the benefit if the primary beneficiary passes away before or at the same time as you. This small step prevents serious legal delays.

To see a broader picture of how life insurance works in the context of overall family security, it helps to think of it not as a product but as a promise. You’re funding a financial guarantee while you’re alive so your family doesn’t have to scramble when you’re gone.

Types of life insurance: term versus whole

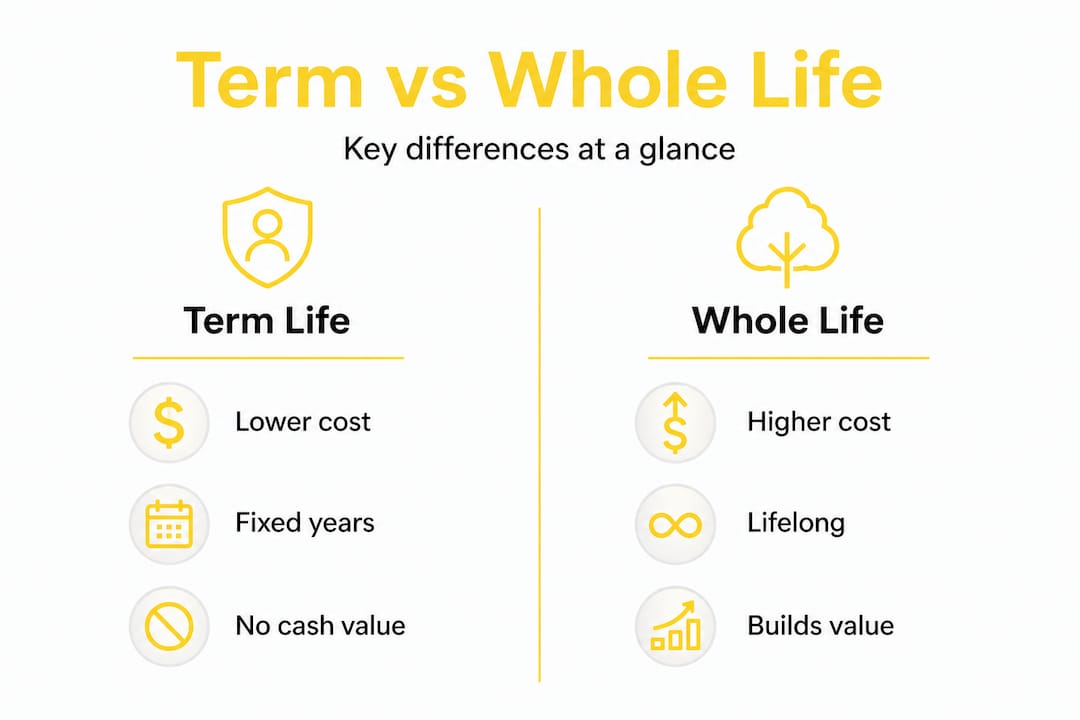

The two primary categories of life insurance are term life and whole life. Both serve a purpose, but they work very differently and attract different types of buyers. Here’s a side-by-side look at what separates them.

Feature | Term life insurance | Whole life insurance |

Coverage length | Fixed period (10, 20, or 30 years) | Lifetime coverage |

Monthly premium | Low (e.g., $25–$48/month for $500K at age 30–40) | Significantly higher |

Cash value | None | Yes, grows over time |

Payout guaranteed | Only if death occurs in term | Yes, whenever you die |

Best for | Young families, income replacement | Lifelong coverage needs, estate planning |

Flexibility | Limited after term expires | Borrow against cash value |

Term life provides coverage for a fixed period of 10 to 30 years, with no cash value and the lowest premiums available. A healthy 30-year-old can get $500,000 in coverage for around $25 to $48 per month. That’s an extremely affordable safety net for families in their peak earning and family-raising years.

Whole life insurance costs considerably more. The trade-off is that you’re buying lifelong coverage and building a cash value component that grows slowly over decades. However, whole life cash value can be borrowed or withdrawn, but doing so reduces the death benefit. The growth rate typically runs between 2 and 4 percent annually, compared to 7 to 10 percent average long-term stock market returns. Many financial advisors point out that buying a term policy and investing the premium difference often produces better results over time.

To go deeper on this decision, reviewing how to compare types of life insurance for your family’s situation can save you from overpaying or underprotecting.

Pro Tip: If you’re under 45 with dependents, a mortgage, and a moderate budget, term life insurance is almost always the smarter starting point. You get the maximum death benefit for the minimum premium during the years your family needs protection most.

There are also other varieties of life insurance worth knowing. Universal life adds flexible premium payments and an adjustable death benefit. Variable life ties cash value growth to market investments. Burial insurance is a small whole life policy designed specifically to cover funeral costs. Each serves a different audience, and you can read more about term life insurance explained in detail to see how the mechanics line up with everyday family needs.

The key takeaway: don’t choose a policy type based on what sounds more impressive. Choose based on how long you need coverage, how much you can pay, and what role you want the policy to play in your overall financial plan.

How the life insurance payout process works

Most people buying life insurance focus on getting covered and then stop thinking about the policy until something actually happens. But understanding the payout process matters because it directly affects how fast and easily your family gets the money they need.

Here’s a general timeline of what happens after a policyholder passes away:

Stage | What happens | Typical timeframe |

Notification | Beneficiary contacts the insurance company | Within days of death |

Claim filing | Beneficiary submits claim form and death certificate | 1–7 days to file |

Review period | Insurer reviews claim and verifies policy terms | 7–30 days |

Payout issued | Beneficiary receives funds | 14–60 days total |

Death benefit payouts work like this: beneficiaries file a claim with the death certificate, and the insurer typically pays a lump sum that is tax-free to the recipient. Other options include installments or an annuity structure, but the lump sum is most common. The entire process generally takes between 14 and 60 days.

For insurance for families, the speed of payout can be just as important as the amount. Families facing mortgage payments, childcare costs, and daily expenses can’t afford a six-month delay.

Here’s what helps ensure a faster, smoother claim:

Keep a copy of your policy in a secure, accessible location that your beneficiaries know about.

Tell your beneficiaries the name of your insurance company and your policy number.

Keep beneficiary information up to date, especially after marriage, divorce, or the birth of a child.

Make sure you haven’t let your policy lapse due to missed premiums.

Avoid causes of death that might trigger exclusions, which we’ll cover in the next section.

“An unclaimed life insurance policy helps no one. Make sure the right people know exactly where to find your policy documents.”

One important note: some policies include a contestability period, usually the first two years after purchase. During this window, the insurer has the right to investigate claims more closely, including reviewing your application for accuracy. If they find misrepresentation, they can deny the claim. After the contestability period, approved claims are almost always paid as long as premiums were current and no exclusions apply.

Choosing the right life insurance policy for your needs

Picking the right policy is where most families get stuck. The process doesn’t have to feel overwhelming if you break it into clear steps.

Assess your family’s financial needs. Start by calculating how much your family would need if your income disappeared tomorrow. Add up annual living expenses, remaining mortgage balance, outstanding debts, estimated college costs, and anticipated funeral expenses. A common rule of thumb is 10 to 15 times your annual income, but your specific number will differ based on your situation.

Choose your coverage amount and term length. For term life, pick a term that covers your most financially vulnerable years. If your youngest child is 3 and you have 22 years left on your mortgage, a 25-year term makes more sense than a 10-year term.

Account for your health, age, and budget. Life insurance premiums are largely based on your age and health at the time of application. The younger and healthier you are, the lower your premiums. Getting covered early locks in better rates.

Compare policies from multiple insurers. Premiums, riders, customer service records, and financial strength ratings all vary. Use your state’s insurance commissioner website or a licensed advisor to compare options. Reviewing comparing insurance policies can help you approach this side by side rather than in isolation.

Be completely honest on your application. This is non-negotiable. Be honest on applications to avoid contestability denial, and review exclusions and riders for specific risks like aviation or hazardous hobbies. Hiding a pre-existing condition to get lower premiums may seem harmless, but it can result in your family’s claim being denied exactly when they need the money most.

Review riders and optional features. Common riders include waiver of premium if you become disabled, accelerated death benefit if you’re diagnosed with a terminal illness, child term riders, and accidental death benefit. Not every rider is worth the cost, but some offer real protection for very little additional premium.

Pro Tip: If you’re unsure how much coverage you need, use the DIME method: add up your Debts, Income replacement (10 years minimum), Mortgage balance, and Education costs for your children. This gives you a concrete baseline coverage number.

A common mistake families make is choosing the cheapest policy without reading what it covers. Price matters, but it’s not the only factor. The goal is to find a policy that fits your budget and actually pays out when your family needs it. Understanding insurance that matters means looking at coverage quality, not just cost.

Our take: Most families need less expensive, simpler coverage and smart honesty matters

Here’s what we believe that most general life insurance articles skip over: the life insurance industry has a strong financial incentive to sell you whole life. Commissions are higher. Policies are more complex and harder to cancel. Customers stay longer. That’s not a judgment. It’s just how the business works.

But for the vast majority of American families, a well-chosen term life policy combined with disciplined investing is a genuinely stronger financial strategy. Term plus investing the difference often outperforms whole life as an investment vehicle, because markets historically return 7 to 10 percent annually compared to 2 to 4 percent growth inside a whole life cash value account. The flexibility you gain by not locking money into a policy also matters during life’s unexpected turns.

We’ve seen families buy $400-a-month whole life policies when a $50-a-month term policy would have given their children the same death benefit with $350 left over each month to build real wealth. The expensive policy felt safer. It wasn’t.

At the same time, we want to be clear: whole life isn’t always wrong. For high-net-worth individuals looking at estate planning, or for people who have lifelong dependents and genuinely need permanent coverage, whole life serves a real purpose. The problem isn’t the product. It’s buying any product that isn’t right for your situation.

The second point we push hard on is honesty during the application. People underestimate how often claims are denied due to application misrepresentation, and they don’t realize this can happen years after the policy was purchased and premiums were faithfully paid. Choosing the right life insurance type is step one, but being completely accurate on your application is what actually protects your family when it counts.

A cheaper, simpler policy that fits your real situation honestly beats an expensive, complicated policy that was built on incomplete information. Every single time.

Get help securing your family’s future

Knowing what to look for is a strong start. Taking action is what actually protects your family.

At Strawderman Financial LLC, our licensed advisors help families across the United States find life insurance guidance that fits their real lives, not a generic template. Whether you’re just starting your coverage search or reconsidering a policy that no longer fits, we can help you compare options, understand your numbers, and make confident decisions. We also offer retirement planning services and wealth accumulation strategies so your protection plan and your long-term financial goals work together. Schedule a free consultation and let us do the heavy lifting on your behalf.

Frequently asked questions

What is the difference between term and whole life insurance?

Term life covers you for a fixed period with lower costs and no cash value, while whole life lasts your entire life and builds cash value but costs significantly more each month.

Who should consider life insurance?

Anyone with loved ones who rely on their income, carry shared debts, or wants to cover final expenses should consider life insurance, regardless of age or income level.

Are life insurance payouts really tax-free?

Yes. Life insurance payouts are generally received as a tax-free lump sum, meaning your beneficiaries keep the full death benefit without owing federal income tax on it.

What happens if I outlive a term life policy?

Term life covers only a fixed period, so if you outlive your policy, coverage ends with no payout. Most insurers offer options to renew or convert to permanent coverage before the term expires.

What could prevent a life insurance claim from being paid?

Dishonesty on applications or unreviewed policy exclusions, such as those covering aviation accidents or certain pre-existing conditions, are the most common reasons a claim gets denied.

Recommended

Comments