What is term life insurance? Protect your family's future

- JF Strawderman

- Apr 16

- 8 min read

TL;DR:

Over 80% of Americans overestimate the cost of term life insurance, leading to undercoverage.

Term life insurance provides affordable, fixed-term protection without cash value, ideal for families.

Many delay purchasing coverage due to confusion and cost fears, risking insufficient protection.

Most Americans think life insurance costs far more than it actually does. In fact, over 80% of Americans overestimate the cost of term life insurance, which means millions of families are going without coverage they could actually afford. That gap between perception and reality is costly, not just financially but for the people you love most. If you’ve been putting off getting covered because you assume it’s out of reach, this guide is for you. We’ll break down exactly what term life insurance is, how it works, how it compares to other options, and how to figure out the right amount for your family.

Table of Contents

Key Takeaways

Point | Details |

Term life is affordable | Most people overestimate the cost, but term life can fit almost any budget. |

Coverage is simple | You choose your coverage years and amount, and if you pass away in that time, your loved ones are protected. |

Match your needs | Estimate 10-15x your income and pick a term length that fits your family’s plans and debts. |

Avoid common mistakes | Don’t underinsure or wait—explore options early for the best rates and protection. |

What is term life insurance?

Term life insurance is one of the simplest forms of life insurance available. It provides coverage for a specific period of time, commonly 10, 20, or 30 years. If the insured person dies during that period, their beneficiaries receive a lump-sum payment called a death benefit. If the term ends and the insured is still alive, the policy simply expires with no payout.

Unlike permanent life insurance products, term life has no cash value component. You’re paying purely for protection, nothing more. That’s what keeps it affordable. Think of it like renting coverage for the years your family needs it most, rather than buying a policy that doubles as an investment account.

Term life is a straightforward policy with set years of coverage, which makes it easy to understand and budget for. Here’s what typically defines a term life policy:

Fixed term length: You choose 10, 15, 20, or 30 years based on your needs.

Level premiums: Your monthly payment stays the same for the entire term.

Death benefit: A set dollar amount paid to your beneficiaries if you die during the term.

No cash value: Unlike whole life, there’s no savings or investment element.

Flexibility: You can often choose coverage amounts from $100,000 to several million dollars.

Who buys term life? Mostly parents with young children, homeowners with a mortgage, and anyone whose family depends on their income. Understanding why families buy life insurance often comes down to one core need: making sure the people who depend on you are protected if the worst happens.

Pro Tip: If you’re in your 20s or 30s, locking in a term policy now means lower premiums for the entire term. Waiting even five years can meaningfully increase your cost.

How does term life insurance work?

Understanding what term life insurance is, let’s walk through exactly how it works. The process is more straightforward than most people expect.

Choose your term length. Decide how many years of coverage you need. A 30-year-old parent might choose a 20-year term to cover their children until they’re independent.

Set your coverage amount. This is the death benefit your family would receive. We’ll cover how to calculate this in a later section.

Apply for coverage. You’ll fill out an application that includes health questions and sometimes a medical exam.

Go through underwriting. The insurance company reviews your health history, age, lifestyle, and other risk factors to determine your premium.

Pay your premiums. Once approved, you make regular payments, usually monthly or annually, to keep the policy active.

Benefit is paid if needed. If you die during the term, your beneficiaries file a claim and receive the lump-sum death benefit, typically tax-free.

Term life insurance pays a death benefit if the insured dies during the coverage period. That payout can be used for anything: replacing lost income, paying off a mortgage, covering college tuition, or handling daily living expenses.

What happens if you outlive the policy? Coverage ends, and no benefit is paid. Some policies offer a renewal option or the ability to convert to a permanent policy, but these options vary by insurer and often come at a higher cost.

One of the biggest advantages of term life is the consistency. Your premium is locked in from day one. No surprises, no rate hikes mid-term. That predictability makes it easy to budget, which is why so many families rely on it to ensure insurance protects your family during their most financially vulnerable years.

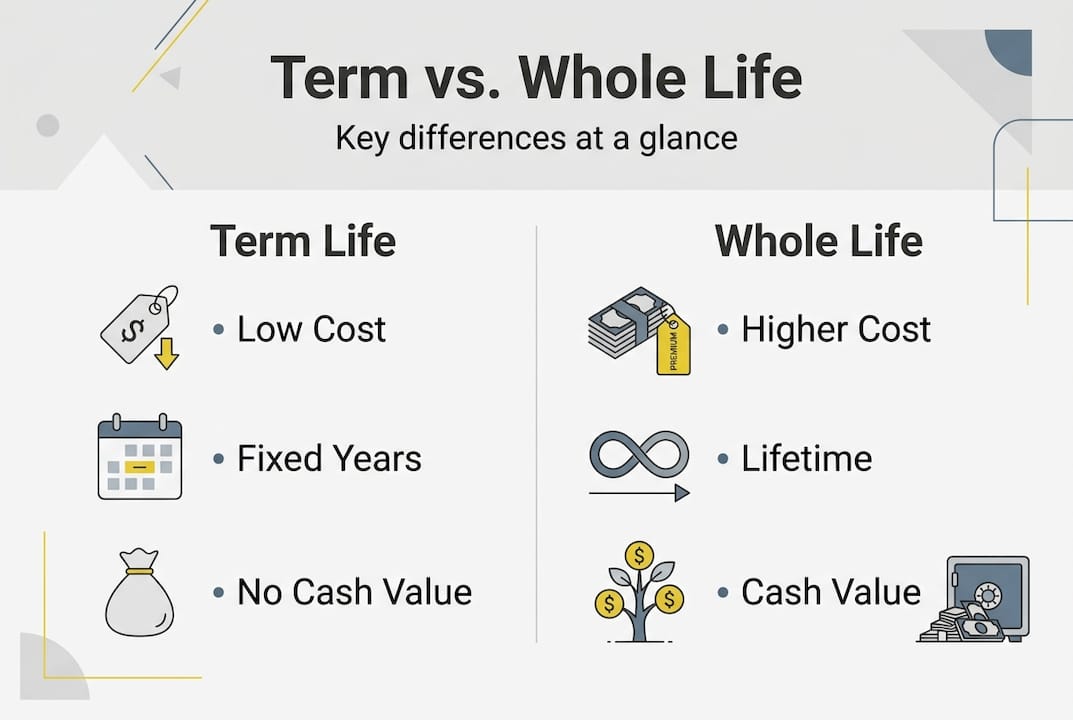

Term vs. whole life insurance: Key differences

Now that you know the mechanics, it’s important to see how term life insurance stacks up against its main alternative. Whole life insurance is a permanent policy that covers you for your entire life and builds a cash value over time. Both serve a purpose, but they’re built for different situations.

Term life is much more affordable than whole life for the same coverage amount. Here’s a side-by-side look:

Feature | Term life | Whole life |

Coverage duration | Fixed term (10-30 years) | Lifetime |

Monthly cost | Lower | Significantly higher |

Cash value | None | Builds over time |

Death benefit | Paid if death occurs in term | Guaranteed payout |

Best for | Income replacement, debt coverage | Estate planning, lifelong needs |

Complexity | Simple | More complex |

Whole life premiums can be 5 to 15 times higher than term life for the same death benefit. That difference is significant for families on a budget. Explore the full range of types of life insurance to understand which fits your situation.

Who typically chooses each?

Term life buyers: Young families, new homeowners, people with temporary financial obligations, anyone who wants maximum coverage at minimum cost.

Whole life buyers: High-income individuals, those with estate planning needs, people who want guaranteed lifelong coverage or a forced savings component.

When comparing insurance options, the right answer depends on your goals. For most families focused on protecting income and paying off debts, term life delivers the most value per dollar.

How much term life insurance do you need?

Clarity about which type to choose still leaves the question: how much do you actually need? This is where many buyers get stuck, and it’s also where underinsurance becomes a real problem. 41% of people believe they have insufficient life insurance coverage.

The most widely used rule of thumb is to carry 10 to 15 times your annual income in coverage. But that’s just a starting point. Your actual number should reflect your specific obligations.

Here’s a simple way to calculate your coverage need:

Add up your income replacement need. Multiply your annual income by the number of years your family would need support.

Include outstanding debts. Add your mortgage balance, car loans, and any other significant debt.

Factor in future expenses. Include estimated college costs for children or other major upcoming expenses.

Subtract existing assets. Deduct savings, existing life insurance, and other liquid assets.

Here’s a quick reference for different family situations:

Family type | Suggested coverage | Suggested term |

Single parent, 2 kids, $60K income | $600,000 to $900,000 | 20 to 25 years |

Dual income, mortgage, $100K combined | $500,000 to $750,000 | 20 to 30 years |

Single, no dependents, $50K income | $250,000 to $500,000 | 10 to 15 years |

Retiree, no dependents | Minimal or none | N/A |

Pro Tip: It’s better to slightly overestimate your coverage. Inflation reduces the real value of a fixed death benefit over time, and life changes like a new child or a larger mortgage can increase your needs. Policies that life insurance protects dependents best are ones sized generously from the start.

Use insurance policy comparison tips to evaluate quotes side by side once you have a target number in mind.

Common mistakes and how to avoid them

Once you estimate your need, avoid the traps that many buyers fall into. These mistakes are common, but they’re also completely preventable.

Assuming it costs too much without checking. Over 80% overestimate term life costs, and 41% feel underinsured as a result. Get an actual quote before assuming coverage is out of reach.

Buying too little coverage. Choosing a lower death benefit to save on premiums often backfires. The monthly savings are small, but the coverage gap can be devastating.

Picking the wrong term length. A 10-year policy might feel sufficient now, but if your youngest child is 5, you may want coverage through their college years and beyond.

Skipping the review after life changes. Marriage, a new baby, a home purchase, or a raise all change your coverage needs. Reviewing your policy annually keeps it aligned with your real life.

Waiting for the perfect moment. Many people delay getting coverage while waiting for a better financial situation. The longer you wait, the older and potentially less healthy you are, which raises premiums.

The best insurance safeguards for families are the ones that are actually in place. You can always adjust coverage later, but you can’t retroactively protect your family.

Pro Tip: Start by getting a free quote online. Even a $250,000 policy can make a meaningful difference for your family, and you may be surprised by how affordable it is. Browse more on insurance risks to stay informed as your needs evolve.

Our take: The term life insurance truth families must not ignore

With the facts and pitfalls in mind, here’s what years of working with families have taught us: the biggest barrier to life insurance isn’t cost. It’s decision paralysis.

Families research, compare, and worry about choosing the perfect policy. Meanwhile, months pass and no coverage is in place. Underinsurance is often a result of confusion and cost overestimation, not actual unaffordability.

Here’s the truth: a simple term policy taken out today is almost always better than a perfectly optimized policy that never gets purchased. Protection now is worth more than getting every single detail right. You can adjust coverage later as your situation changes. What you can’t do is go back in time.

We’ve seen families who spent years comparing options end up with nothing when it mattered most. Don’t let that be your story. Take one small step today, whether that’s getting a quote, reviewing your current coverage, or simply learning more about securing your family’s future. Progress beats perfection every single time.

Take your next step toward protection

You now have the knowledge to make a confident decision about term life insurance. The next move is yours.

At Strawderman Financial, we specialize in helping families like yours find the right coverage at a price that works. Whether you’re exploring life insurance solutions for the first time or looking to update existing coverage, our agents walk you through every option without the pressure. We also offer financial planning services to help you see the full picture, from income protection today to retirement security tomorrow. Schedule a free consultation and let us help you build a plan that actually fits your life.

Frequently asked questions

What happens if I outlive my term life insurance?

If you outlive your term life insurance, coverage simply ends and no benefit is paid, but you may have options to renew or convert to a permanent policy depending on your insurer.

How much does term life insurance cost on average?

Most people overestimate term life insurance costs by more than three times the actual price, making it far more affordable than most families assume.

Can I get term life insurance if I have pre-existing health conditions?

You can often still qualify for coverage, but underwriting considers health history for approval, which may result in higher premiums or fewer policy options.

Is term life insurance better for families than whole life?

Term life is much more affordable and fits most families’ needs by providing higher coverage amounts for a lower monthly cost compared to whole life.

How do I choose the right coverage amount?

Aim for 10 to 15 times your annual income, or prioritize your longest financial needs such as a mortgage payoff or your children’s education costs.

Recommended

Comments