What is dental insurance? A clear guide to coverage & savings

- JF Strawderman

- Apr 17

- 8 min read

TL;DR:

Dental insurance is separate from health coverage and mainly covers preventive and major oral care.

Various plans like PPOs, HMOs, and discount plans offer different coverage, costs, and provider options.

Having dental insurance encourages regular visits, preventing costly procedures and protecting your budget.

Most Americans assume their health insurance has their teeth covered. It doesn’t. Standard health plans treat your mouth as a separate system, which means routine cleanings, fillings, and crowns come straight out of your pocket unless you have a dedicated dental policy. A single root canal can run over $1,000 without coverage, and a crown can push past $1,500. For families, these surprise bills add up fast. This guide breaks down what dental insurance actually is, how it works, what it covers, and how to choose the right plan so you can protect both your smile and your budget.

Table of Contents

Key Takeaways

Point | Details |

Dental insurance is separate | Dental insurance is distinct from health insurance and covers specific oral health needs. |

Plan types matter | Understanding PPOs, HMOs, and discount plans can help you pick the best dental coverage. |

Maximize preventive care | Most plans cover checkups and cleanings, so use these benefits to prevent bigger bills. |

Budget impact | Dental insurance helps manage costs for both routine care and unexpected procedures. |

Smart planning pays off | Choosing and using dental insurance wisely protects your health and your finances. |

Understanding dental insurance: The essentials

Dental insurance is a standalone policy designed specifically to help you pay for oral healthcare. It is separate from your medical health plan and covers a different set of services. Understanding how health insurance works makes it easier to see why dental needs its own dedicated coverage.

Most dental plans organize coverage into three tiers:

Preventive care (cleanings, X-rays, exams): Usually covered at 100%

Basic services (fillings, extractions, simple repairs): Typically covered at 70-80%

Major services (crowns, root canals, dentures): Often covered at 50%, sometimes less

Like any insurance policy, dental plans have specific financial terms you need to know. Your premium is the monthly amount you pay to keep the policy active. Your deductible is the amount you pay out-of-pocket before your insurance kicks in. The annual maximum is the total dollar amount your insurer will pay in a given year, often between $1,000 and $2,000. Once you hit that ceiling, you pay 100% of remaining costs yourself.

Many plans also include waiting periods, meaning you may need to be enrolled for 6 to 12 months before the plan covers major procedures. This catches a lot of people off guard, especially those who sign up right before a big procedure. Regular dental visits are crucial for preventing costly procedures, which is exactly why understanding your plan before you need it matters so much.

Pro Tip: Before enrolling in any dental plan, request a full schedule of benefits. Look specifically for what is excluded, what has waiting periods, and whether your preferred dentist is in-network. Surprises in dental coverage almost always cost money.

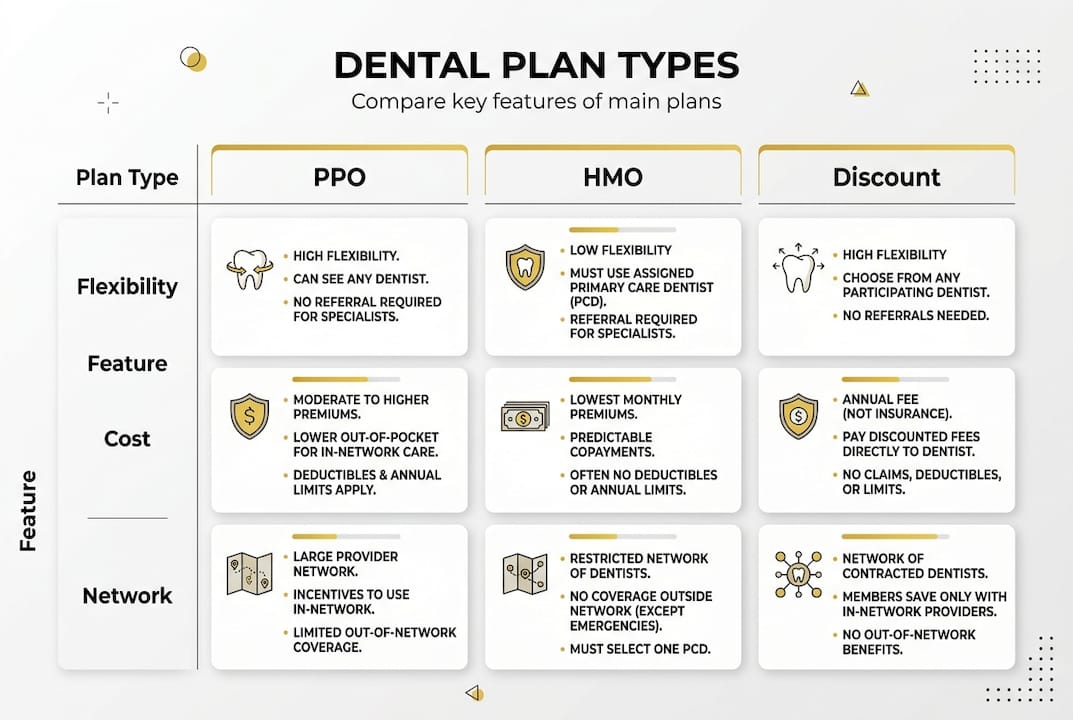

Types of dental insurance plans

With a foundation for how dental insurance works, it’s important to compare the types of plans to find your best fit. PPOs, HMOs, and discount dental plans are the three main types available in the U.S., and each works very differently.

Feature | PPO | HMO | Discount Plan |

Monthly premium | Higher | Lower | Lowest |

Provider flexibility | High | Low | Moderate |

Deductible | Yes | Usually none | None |

Annual maximum | Yes | Yes | None |

Waiting periods | Possible | Possible | None |

Best for | Flexibility seekers | Budget-focused | Uninsured individuals |

PPO (Preferred Provider Organization) plans let you visit any licensed dentist, though you pay less when you stay in-network. They offer the most flexibility but come with higher premiums.

HMO (Health Maintenance Organization) dental plans require you to choose a primary dentist and get referrals for specialists. They cost less monthly but limit your provider options significantly.

Discount dental plans are not insurance at all. They are membership programs that give you reduced rates at participating dentists. There are no claims, no deductibles, and no annual maximums, but you pay the discounted rate yourself at every visit.

Here is a quick breakdown of what to consider:

Families with kids who need orthodontics may benefit from a PPO with orthodontic riders

Individuals on tight budgets who rarely need major work might do well with an HMO or discount plan

Self-employed people without employer benefits should compare group vs individual insurance carefully before choosing

If your employer offers dental as a group benefit, compare the cost and coverage to individual market options before defaulting to it

Understanding insurance plan terms explained in plain language helps you evaluate each plan type without getting lost in the fine print.

Dental insurance versus health insurance: Key differences

Knowing your plan options is key, but understanding how dental insurance stands apart from health insurance helps you avoid costly mistakes. Here is a side-by-side look at the core differences:

Feature | Dental insurance | Health insurance |

Covered services | Cleanings, fillings, crowns, root canals | Doctor visits, hospital stays, prescriptions |

Deductible | $50 to $150 typically | $500 to $2,000+ typically |

Annual maximum | $1,000 to $2,000 | Usually no cap on benefits |

Copays | Common for each visit | Common for office visits |

Provider network | Separate dental network | Medical provider network |

Here are the big-picture takeaways every family should know:

Dental insurance covers preventive and routine oral care. Health insurance only steps in for oral issues tied to trauma or medically necessary surgery.

The two plans use completely separate provider networks. Your medical doctor and your dentist operate in different systems.

Dental emergencies are not reliably covered by health insurance. A broken tooth from an accident might get partial coverage, but a standard toothache will not.

Annual maximums in dental plans are low. If you need multiple major procedures in one year, you can hit your cap quickly.

Over 40% of Americans mistakenly believe their medical insurance pays for all dental care. That misunderstanding leads to skipped appointments and financial shock when bills arrive.

Pro Tip: Pull out your health insurance summary of benefits and search for “dental.” Most plans cover only emergency extractions or oral surgery tied to a medical diagnosis. Do not rely on your health insurance options to fill dental gaps without confirming the details first. Reviewing health insurance types can also help you understand where dental fits into your overall coverage picture.

How dental insurance impacts your budget and health

Grasping the difference between dental and health insurance helps you see why having dental coverage can really matter for your wallet and wellbeing. Dental insurance is not just about saving money on cleanings. It is about preventing the kind of expensive, painful problems that develop when small issues go untreated.

People with dental insurance are twice as likely to get regular cleanings as those without. That statistic matters because a $150 cleaning can prevent a $1,200 root canal. The math is straightforward.

“Investing in preventive dental care today is one of the most cost-effective health decisions a family can make. The cost of prevention is almost always a fraction of the cost of treatment.”

Here are practical steps to maximize your dental plan’s value:

Schedule both cleanings every year. Most plans cover two preventive visits at 100%. Use them.

Know your plan year reset date. Benefits often reset January 1. Timing major work around this can double your available coverage.

Ask your dentist for a pre-treatment estimate. Before agreeing to any major procedure, get a written estimate of what your plan will pay versus what you owe.

Use your deductible strategically. If you hit your deductible early in the year, try to schedule other needed work before the year ends.

Watch for oral health signals. Dentists can spot early signs of diabetes, heart disease, and nutritional deficiencies. Your mouth is a window to your overall health.

Pro Tip: Treat your preventive dental benefits like a subscription you have already paid for. Skipping a cleaning because you feel fine is leaving money on the table and risking a larger bill later. Explore personal finance tips to see how dental planning fits into a broader financial wellness strategy.

A smarter path to protecting your smile and your budget

Here is something we see repeatedly in financial planning conversations: people skip dental coverage because the monthly premium feels like an unnecessary expense. Then a crown or an emergency extraction hits, and suddenly that $35 monthly premium looks like the best investment they never made.

The real value of dental insurance is not always in what you get reimbursed. It is in the care you actually show up for. When people have coverage, they go to the dentist. When they go to the dentist, small problems get caught early. That is the cycle that saves real money over time.

Annual maximums and waiting periods are the two features that most often catch families off guard. If you enroll in a plan expecting to get a crown next month, you may be disappointed. Planning ahead, ideally before you have an urgent need, is the smarter move.

Think of dental coverage as part of your family’s health budget, not an optional add-on. When you are comparing insurance for future needs, dental belongs in the same conversation as life, health, and supplemental coverage. It is not a luxury. It is a practical tool for managing predictable costs.

Ready to safeguard your health and finances?

Understanding dental insurance is a strong first step, but the real protection comes from having the right plan in place before you need it.

At Strawderman Financial, we help individuals and families across the United States find dental, health, and life coverage that fits their real lives and real budgets. Whether you are starting from scratch or reviewing what you already have, our advisors make the process straightforward. Explore health insurance options alongside dental, or take a closer look at life insurance plans to build a complete safety net. Connect with our trusted insurance advisors today for a free consultation and start planning with confidence.

Frequently asked questions

Does dental insurance cover braces and orthodontics?

Most dental plans cover orthodontics for children, but adult coverage varies widely and often includes age or spending limits. Always confirm orthodontic benefits and lifetime maximums before enrolling.

Can I buy dental insurance at any time of year?

Yes. Unlike health insurance, dental plans are available outside of open enrollment since they are not governed by the Affordable Care Act. You can typically enroll year-round.

Is preventive care always free with dental insurance?

Most dental plans cover preventive services at 100%, but some plans apply a deductible or require you to use in-network providers to get full coverage.

How do I find a dentist in my dental plan network?

Visit your insurer’s website and use the provider search tool, or call the customer service number on your insurance card to get a list of in-network dentists near you.

What if I need a major treatment right away?

Many dental plans impose waiting periods for major procedures, sometimes 6 to 12 months. Review the plan’s waiting period rules carefully before enrolling if you have an immediate treatment need.

Recommended

Comments