Life insurance medical exams: what to expect and how to prepare

- JF Strawderman

- May 4

- 10 min read

TL;DR:

Modern underwriting often skips traditional exams, using electronic health data for approvals.

A medical exam assesses risk, discovers undiagnosed conditions, and determines accurate premiums.

Proper preparation and honesty can improve exam results and lead to better insurance rates.

Many people assume getting life insurance means submitting to a full physical at a doctor’s office, complete with blood draws, lengthy paperwork, and weeks of waiting. That assumption stops a lot of people from ever applying. The reality is far less intimidating. Accelerated underwriting now skips the traditional exam for many healthy applicants, using data sources to match the rates you’d get through a full exam. This guide walks you through exactly what the medical exam process involves, how to prepare, and when you might not need one at all.

Table of Contents

Key Takeaways

Point | Details |

Not always required | Many applicants can qualify for life insurance without a medical exam thanks to accelerated underwriting. |

Preparation matters | Simple habits before your medical exam can significantly improve your chances of securing better rates. |

Alternatives exist | No-exam and accelerated underwriting options offer fast approval, especially for healthy applicants. |

Results impact pricing | Exam results directly affect your life insurance cost and eligibility, so accuracy and preparation are crucial. |

Expert guidance helps | Consulting with a knowledgeable adviser ensures you choose the best life insurance path for your needs. |

Why do life insurance companies require a medical exam?

Life insurance is a financial promise. The insurer agrees to pay a death benefit, sometimes millions of dollars, based on how long they estimate you’ll live. To make that calculation accurately, they need real health data. Without it, they’d either charge everyone higher premiums to cover the unknown risk, or lose money on policies priced too low for high-risk individuals.

The medical exam exists to make pricing fair. A 35-year-old nonsmoker in excellent health shouldn’t pay the same rate as someone managing multiple chronic conditions. The exam gives insurers the data they need to separate those risk categories and price policies accordingly. It benefits healthy applicants directly, because good health translates to lower premiums.

Here’s what the traditional exam accomplishes:

Risk assessment: Insurers can categorize you into health classes such as Preferred Plus, Preferred, Standard, or Substandard, each carrying a different premium level.

Condition discovery: Some applicants have undiagnosed conditions, like high blood pressure or elevated blood sugar, that show up in lab work for the first time.

Fraud prevention: Self-reported health histories can be incomplete or inaccurate. Lab results provide objective confirmation.

Premium accuracy: The data collected during your exam sets the price for your entire policy term, sometimes 20 or 30 years.

“The exam isn’t designed to disqualify you. It’s designed to place you in the right risk category so your premiums reflect your actual health. For healthy applicants, that’s usually a very good thing.”

That said, the industry is evolving. Understanding life insurance underwriting helps clarify why some companies are now moving toward data-driven approvals that skip the physical altogether. Electronic health records, prescription databases, and credit-based insurance scores give insurers enough information to make underwriting decisions without a single needle stick.

What happens during the medical exam?

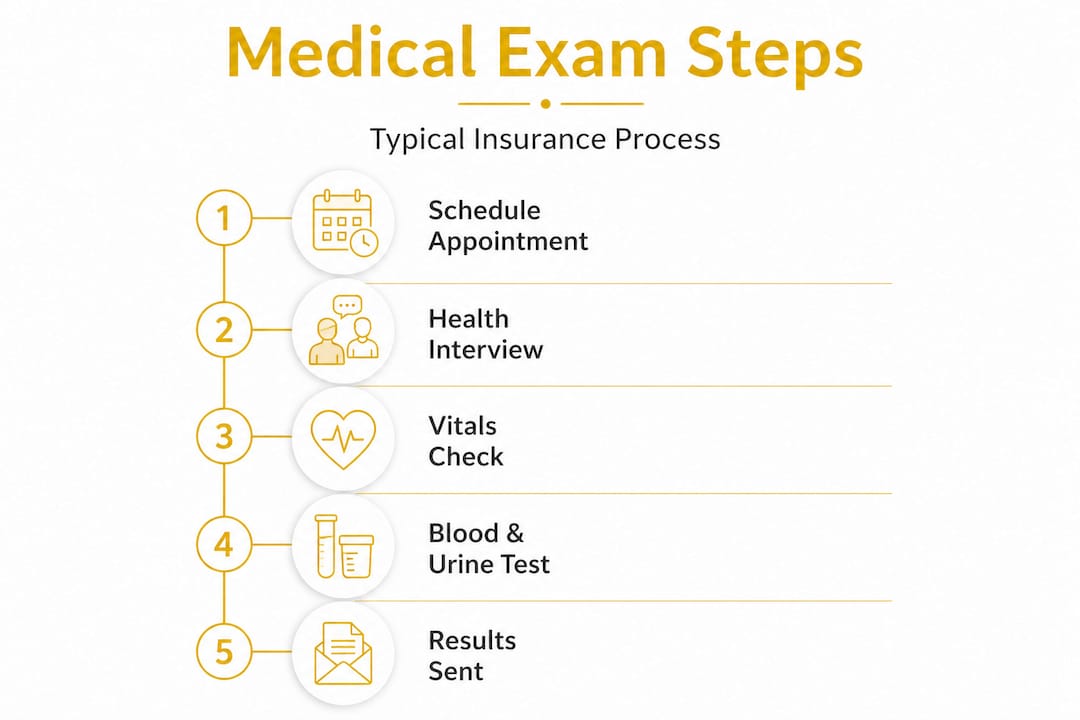

The insurance medical exam is not the same as a visit to your doctor. It’s shorter, more focused, and usually performed by a paramedical professional at your home or workplace at no cost to you. Here’s the typical sequence:

Schedule your appointment. After submitting your application, the insurance company arranges the exam through a third-party paramedical service. You choose a time and location that works for you.

Confirm your identification. Bring a valid government-issued photo ID such as a driver’s license or passport. You’ll also need your insurance application reference number.

Complete a health history interview. The examiner will ask about your medical history, current medications, past surgeries, family health history, and lifestyle habits like smoking or alcohol use.

Undergo physical measurements. Height, weight, and blood pressure are recorded. These numbers directly influence your risk classification.

Provide blood and urine samples. This is the most clinically significant part of the exam. The blood draw is usually just one or two small vials.

Complete any additional tests if required. For older applicants or higher coverage amounts, you may also have an electrocardiogram (EKG) to evaluate heart function, or a saliva swab for nicotine testing.

The entire appointment typically takes between 20 and 30 minutes. Results are sent directly to the insurer, not to you automatically, though you can usually request them.

Pro Tip: Schedule your exam for early morning if possible. Fasting beforehand is often required for accurate blood glucose readings, and morning appointments make that much easier to manage.

One thing worth emphasizing: your honesty during the health history interview matters enormously. Misrepresenting your medical history can void your policy later, leaving your family with nothing when they need it most. The whole point of applying for coverage is protecting loved ones, and that protection only holds if the policy is issued on accurate information.

What is tested, and what are insurers looking for?

Once the exam is underway, here’s what will be checked and why it matters for your policy.

The blood and urine samples are analyzed for a specific set of health markers. Each one tells the insurer something different about your current health and long-term risk profile.

Test | What it measures | Why insurers care |

Cholesterol panel | Total, HDL, LDL, triglycerides | High LDL or low HDL signals cardiovascular risk |

Blood pressure | Systolic and diastolic readings | Hypertension is a major mortality risk factor |

Blood glucose | Fasting blood sugar levels | Elevated levels may indicate diabetes or pre-diabetes |

Complete blood count | Red/white cells, hemoglobin | Detects anemia, infections, or blood disorders |

Kidney function | Creatinine, BUN levels | Chronic kidney disease affects life expectancy |

Liver function | ALT, AST enzymes | Elevated levels can signal alcohol use or liver disease |

Nicotine/cotinine | Tobacco product use | Smokers typically pay 2 to 3 times more than nonsmokers |

Drug screening | Illicit substance use | Positive results can lead to declination |

Beyond the lab numbers, here are the key red flags that underwriters look for:

Chronic conditions such as heart disease, diabetes, cancer history, or COPD (chronic obstructive pulmonary disease)

Tobacco or drug use, whether disclosed or detected through testing

Abnormal organ function that suggests underlying disease

Obesity, particularly when combined with other risk factors like high blood pressure

Family history of early heart disease or cancer, which may still affect your classification

Understanding how life insurance works helps you see why these metrics matter so much. The accelerated underwriting trend exists precisely because these same data points can often be gathered from electronic records, making a physical exam less necessary for lower-risk applicants.

The outcome of your exam doesn’t always mean approval or denial. It means classification. A clean bill of health often unlocks the best available rate class, which saves you real money over a 20 or 30-year policy term. When comparing life insurance types, keep in mind that exam-based policies almost always offer lower premiums than no-exam alternatives for healthy individuals.

Exemptions and alternatives: do you really need a medical exam?

But what if you want to avoid the hassle of lab work? Here’s when and how you might skip the medical exam altogether.

The insurance industry has invested heavily in accelerated underwriting, a process that replaces the physical exam with a combination of digital data sources. These include electronic health records, prescription history databases, the MIB (Medical Information Bureau) database, motor vehicle reports, and credit-based insurance scores. For many applicants, this data paints an equally accurate picture of health risk without a single lab result.

Here’s how traditional exams compare to no-exam alternatives:

Feature | Traditional exam | Accelerated/no-exam |

Required lab work | Yes | No |

Application decision time | 2 to 8 weeks | Hours to a few days |

Premium cost | Lower for healthy applicants | Slightly higher on average |

Coverage amounts available | Up to several million dollars | Often capped at $1 to $3 million |

Best for | Healthy individuals, large policies | Younger/healthy, convenience seekers |

Age eligibility | All ages | Typically under 60 |

To qualify for accelerated underwriting, you generally need to be in good health, have no major chronic conditions, and be applying for a coverage amount within the insurer’s no-exam threshold. Most companies cap this between $500,000 and $3 million, though thresholds vary.

No-exam policies also include guaranteed issue and simplified issue options. Guaranteed issue requires no health questions at all, making it accessible to people with serious medical conditions, but premiums are significantly higher and death benefits are usually capped at $25,000 to $50,000. Simplified issue asks a few basic health questions but skips the lab work.

Pro Tip: If you’re under 45 and in good health, ask your agent specifically about accelerated underwriting eligibility before scheduling an exam. You may qualify for comparable rates with far less hassle, and decisions can sometimes come back within 24 hours.

The key reasons why buy life insurance apply regardless of which exam path you take. The goal is to get covered, and modern tools mean more ways than ever to do that efficiently.

How to prepare and maximize your results

No matter which exam path you take, a little preparation goes a long way. Here’s what you can do to ensure the best outcome.

The days leading up to your exam can genuinely affect your results. Blood pressure, blood glucose, and cholesterol readings are all sensitive to recent behaviors. Small changes in the 48 to 72 hours before your exam can make a meaningful difference.

Here’s your preparation checklist:

Fast for 8 to 12 hours beforehand if your exam includes blood glucose testing. Drink water but avoid food, coffee, and juice.

Avoid alcohol for at least 24 hours before the exam. Alcohol raises triglycerides and can affect liver enzyme readings.

Skip intense exercise the day before. Vigorous workouts temporarily raise certain enzymes that may look problematic on a blood test.

Reduce sodium intake for 48 hours ahead of time. High sodium can spike blood pressure readings temporarily.

Get 7 to 8 hours of sleep. Poor sleep elevates cortisol and blood pressure.

Drink plenty of water. Staying hydrated makes the blood draw easier and supports cleaner urine samples.

Bring a complete medication list. Include dosages and the conditions each medication treats.

Bring valid photo ID. A driver’s license or passport is standard.

Honesty throughout the process protects you. If you have pre-existing conditions and fail to disclose them, the insurance company can legally deny a claim later on those grounds. That’s a worst-case scenario for your family and entirely avoidable.

One thing most applicants overlook: your insurance tips should include reviewing your prescription history before the exam. Insurers check prescription databases, and an old prescription for a medication you no longer take can raise questions if it’s not explained upfront. Being prepared to discuss your medication history clearly and calmly actually builds credibility with underwriters.

The accelerated underwriting path requires similar honesty during any online health interview. Algorithms cross-reference your answers against prescription records and medical databases, so inconsistencies get flagged.

Rethinking medical exams: what most life insurance shoppers miss

Here’s a candid view you won’t hear in most insurance guides.

Most articles about life insurance medical exams focus on how to avoid them. That framing misses a critical point: for healthy applicants, the traditional exam is often your best financial tool, not your enemy. It’s the one place in the entire insurance process where your good health works unambiguously in your favor.

Think about it this way. A no-exam policy prices in uncertainty. The insurer doesn’t know your exact health status, so they charge a small premium to cover that unknown. If you’re healthy, you’re subsidizing that uncertainty for nothing. A traditional exam removes that uncertainty and rewards you with lower rates. For a 20-year term policy, that difference can amount to tens of thousands of dollars over the life of the policy.

The no-exam revolution is genuinely valuable for people who prioritize speed, have moderate coverage needs, or have certain health conditions that would benefit from simplified underwriting. But it’s not universally the smarter financial move.

What we see at Strawderman Financial is that clients who understand both paths make better decisions. They don’t reflexively avoid exams out of fear or inconvenience. They ask the right question: which path gives me the best coverage at the best price given my specific health profile?

The long-term trajectory of this industry does point toward fewer exams. Data-driven approvals will likely become the standard within the next decade. But right now, in 2026, accelerated underwriting still carries a slight rate premium in most cases for comparable coverage. That gap is narrowing, but it hasn’t closed.

One more thing worth saying plainly: if you’ve been putting off getting life insurance because you’re afraid of what an exam might find, that fear is costing your family real security. Conditions like elevated blood sugar or high cholesterol are manageable, and critical illness insurance options exist specifically for people navigating complex health situations. Don’t let the exam process be the reason your family goes unprotected.

Ready to secure your policy? Explore your life insurance options

If you’re ready to turn knowledge into action, the next step is simple.

At Strawderman Financial, we work with families and individuals across the United States to find life insurance coverage that fits their health profile, budget, and goals. Whether you’re a healthy applicant looking to qualify for the best rates through traditional underwriting, or someone exploring no-exam alternatives for speed and convenience, our experienced agents guide you through every step.

Explore your life insurance options and find out what you qualify for today. If you’re also thinking about the bigger picture, our retirement planning services help ensure your financial security extends well beyond your working years. Schedule a free consultation and let us do the heavy lifting so you can focus on what matters most: protecting the people you love.

Frequently asked questions

How long does the medical exam for life insurance take?

Most exams take 20 to 30 minutes and are usually performed at your home or workplace by a licensed paramedical professional at no cost to you.

Can I still get life insurance if I have pre-existing conditions?

Yes, many applicants with pre-existing conditions still qualify for coverage, though your rates may be higher or additional documentation may be required. No-exam policies and simplified issue options may also be available depending on the condition.

Are the exam results shared with my employer or doctor?

No. Your exam results are confidential and used exclusively by the insurance company for underwriting purposes. They are not reported to your employer, physician, or any outside party.

What if I fail the medical exam?

“Failing” doesn’t always mean denial. You may be offered a higher premium reflecting your risk class, a modified policy with adjusted terms, or the opportunity to retest after demonstrating health improvements. Accelerated underwriting alternatives may also remain available depending on the specific findings.

Recommended

Comments