Retirement Planning Guide: Secure Your Future After 50

- JF Strawderman

- Apr 24

- 8 min read

TL;DR:

Most Americans’ retirement savings are far below recommended levels, creating a financial shortfall.

Maximizing catch-up contributions and strategic Social Security timing can significantly boost retirement income.

Effective income planning focuses on reliable monthly cash flow rather than just reaching savings targets.

The average American approaching retirement holds about $87,000 in savings, enough to last roughly four to five years at a standard withdrawal rate. With retirements commonly stretching 20 to 30 years, that gap is not just uncomfortable, it is a financial emergency waiting to happen. If you are 50 or older, the decisions you make right now carry more weight than almost anything else you have done financially. This guide walks you through a clear, realistic path: assessing where you stand today, boosting your savings fast, timing Social Security wisely, and building a withdrawal plan that lasts as long as you do.

Table of Contents

Key Takeaways

Point | Details |

Most aren’t saving enough | The typical 50+ American falls short of retirement savings benchmarks, risking income gaps. |

Catch-up contributions boost savings | Maximizing 401(k) and IRA extras after 50 can meaningfully increase your retirement funds. |

Social Security timing is crucial | Choosing when to claim Social Security can increase your total retirement income by over $100,000. |

Tax-smart withdrawals stretch your money | Coordinating account withdrawals and understanding the 4% rule helps make savings last. |

Flexible planning beats simple rules | Personalized, adaptable strategies offer the best path to financial security in retirement. |

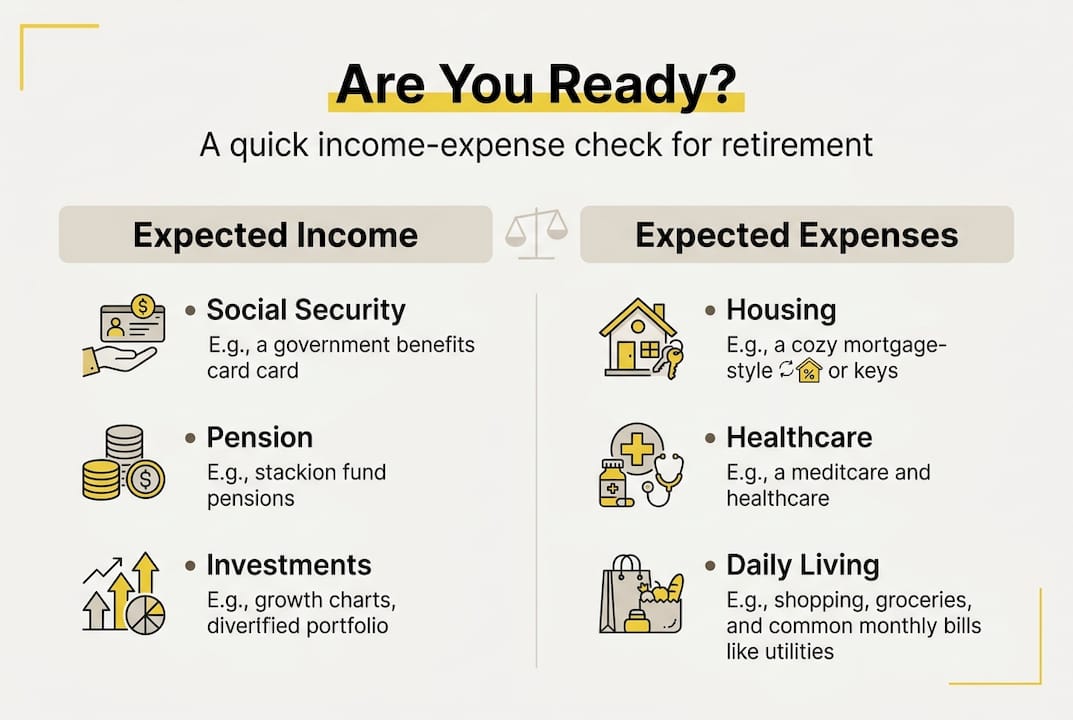

Assessing your retirement readiness

Before you can fix a problem, you need to see it clearly. Start by adding up every source of income you expect in retirement: Social Security estimates (available at ssa.gov), any pension payments, expected withdrawals from 401(k) or IRA accounts, rental income, and any part-time work you plan to do. Then list your expected monthly expenses, and be honest. Most people underestimate what they spend.

Once you have both numbers, compare them. If your expected income falls short of your expected expenses, that shortfall is your income gap. Closing it is the entire point of retirement planning.

Here is how common savings benchmarks compare to what most Americans actually hold:

Age | Fidelity benchmark (savings target) | Median actual savings |

50 | 6x annual salary | Much lower |

55 | 7x annual salary | Much lower |

60 | 8x annual salary | Much lower |

67 | 10x annual salary | Much lower |

The gap between what Fidelity recommends and what most people actually have is striking. Median DC savings represent just a fraction of target amounts, making it essential to act now rather than later.

Your income in retirement will likely come from these sources:

Social Security: Often the largest single income source for Americans

401(k) or IRA withdrawals: Your personal savings engine

Pension payments: Less common today but still relevant for some workers

Taxable brokerage accounts: Flexible, no required distribution age

Real estate or rental income: Can provide steady monthly cash flow

Exploring retirement savings strategies now can help you make the most of whatever you have already built.

Pro Tip: Do not underestimate healthcare costs. Fidelity estimates the average retired couple needs over $300,000 for medical expenses in retirement, and that figure does not include long-term care. Budget for both.

Maximizing savings and catch-up contributions after 50

With a clear view of where you stand, your next task is strengthening your retirement accounts, and it is not too late to make a big impact. Congress created catch-up contributions specifically because people in their 50s and 60s need an accelerated runway.

In 2026, the rules favor older savers in a meaningful way. The 401(k) catch-up limit is $7,500 extra per year for those 50 and older, on top of the standard contribution. IRA holders get an extra $1,000 above the regular limit. These additions can significantly grow your balance over a decade.

Here is a comparison of standard versus catch-up contribution limits for 2026:

Account type | Standard limit (2026) | Catch-up (50+) | Total possible |

401(k) | $23,500 | $7,500 | $31,000 |

IRA | $7,000 | $1,000 | $8,000 |

Roth IRA | $7,000 | $1,000 | $8,000 |

Note: Those aged 60 to 63 may qualify for an even higher 401(k) catch-up under SECURE 2.0 rules, worth checking with your plan administrator.

Follow these steps to maximize savings in your 50s and early 60s:

Maximize your 401(k) contribution to the full catch-up limit first, especially if your employer matches.

Open or fund a Roth IRA if your income qualifies, for tax-free growth.

Pay down high-interest debt aggressively to free up cash for investing.

Redirect any raises, bonuses, or paid-off loan payments directly into savings.

Review your asset allocation to ensure it still matches your timeline and risk tolerance.

Choosing between account types matters just as much as how much you contribute. Understanding insurance for retirement alongside your investment choices helps you build a more complete financial picture. Reviewing your wealth accumulation strategies with a professional can reveal gaps you might not see on your own.

Pro Tip: Consider Roth conversions now while your income may be lower than it will be when required minimum distributions (RMDs) kick in at age 73. Converting portions of your traditional IRA to a Roth reduces your future taxable income and gives you more flexibility later.

Smart Social Security strategies and timing decisions

After maximizing your nest egg, the next pillar is Social Security, a decision that is more nuanced than most people realize. The single biggest mistake many retirees make is claiming benefits too early, locking in a permanently reduced payment that haunts them for decades.

Your claiming age has a dramatic effect on your lifetime income. Consider these key facts:

Claiming at 62 reduces your benefit by roughly 30% compared to your full retirement age (FRA)

Claiming at your FRA (66 or 67 for most people today) gives you 100% of your earned benefit

Delaying to 70 adds approximately 8% per year past your FRA, with no additional gain beyond age 70

The total lifetime difference between claiming at 62 versus 70 can exceed $100,000

Worth knowing: A retiree with a $2,000 monthly benefit at FRA would receive only $1,400 at 62 but $2,480 at 70. Over a 20-year retirement, the delay strategy pays out significantly more, assuming good health.

Factors to weigh carefully when timing your claim:

Your current health and family history of longevity

Whether you have a spouse who may benefit from your higher earnings record

Whether you can cover living expenses without Social Security while you wait

Your other income sources and how they interact with Social Security taxation rules

How NIRS retirement insights show Social Security is the dominant income source for most retirees

Building comprehensive financial planning around your Social Security strategy, rather than treating it as an afterthought, is one of the highest-value moves you can make in your 50s and early 60s.

Creating a tax-savvy and sustainable income plan

Your final step brings all the pieces together: designing a withdrawal strategy that funds your needs and minimizes taxes. Most retirees overlook how much of their savings can disappear to taxes if they pull from accounts in the wrong order.

The standard withdrawal sequence recommended by financial planners follows this logic: taxable accounts first, then traditional (tax-deferred) accounts, and Roth accounts last. This approach lets your Roth savings grow tax-free as long as possible. The 4% safe withdrawal rule, based on the Trinity Study, suggests withdrawing 4% of your portfolio in year one, then adjusting for inflation annually. It is a useful starting point, though not a guarantee.

Here is how a $500,000 portfolio might look under this withdrawal approach over time:

Year | Starting portfolio | Annual withdrawal (4%) | Ending portfolio (estimated) |

1 | $500,000 | $20,000 | $492,000 |

5 | $465,000 | $21,600 | $455,000 |

10 | $420,000 | $23,900 | $408,000 |

20 | $310,000 | $29,000 | $292,000 |

Results vary based on market returns and inflation. This table assumes modest average growth.

Follow these steps to build your withdrawal plan:

Estimate your annual spending needs and identify which accounts will fill each gap.

Determine which accounts to draw from first based on tax impact.

Plan for RMDs at age 73 to avoid penalties and unnecessary tax spikes.

Revisit your plan each year and adjust withdrawals based on portfolio performance.

Coordinate with Social Security and any pension income to avoid bracket creep.

Understanding healthcare costs and planning is essential here too, because medical expenses in retirement can derail even well-designed income plans.

Pro Tip: If you give to charity, qualified charitable distributions (QCDs) allow those 70½ or older to send up to $105,000 directly from an IRA to a charity, satisfying your RMD while keeping that amount out of your taxable income entirely.

A new mindset for retirement: Why the old savings targets fall short

Having explored the critical elements of retirement planning, it is time to look past the numbers and share something most guides leave out. Savings targets and rules of thumb create a false sense of security. Hitting a number on paper feels like victory, but a balance sheet does not pay your heating bill in January.

The real question is not “How much have I saved?” but “How reliably can I generate income every month for 25 or 30 years?” That shift in thinking changes everything. Social Security remains dominant as the primary income source for most retirees, which means your claiming strategy carries enormous weight.

We have seen clients with $400,000 saved feel anxious every month and others with $200,000 feel secure, because the second group built predictable, reliable income streams. The anxious group had assets. The secure group had a plan. Adapting to longer lifespans, rising healthcare costs, and uncertain Social Security futures requires flexibility, not just a target number. Comprehensive planning advice built around income, not just accumulation, is what truly protects your retirement.

Take the next step with expert retirement planning

After rethinking your approach, you may want help putting your plan into action. A personalized retirement income plan considers every piece of your financial life together: your savings, your Social Security timing, your tax situation, and your insurance coverage.

At Strawderman Financial LLC, we specialize in helping Americans 50 and older close income gaps and build retirement security. Our retirement planning services connect you with dedicated agents who listen first and recommend second. If you are also looking at coverage gaps, we can help you explore life insurance options that complement your retirement plan. Reach out today for a free consultation and take the first step toward a retirement you can count on.

Frequently asked questions

How much should I have saved for retirement by age 60?

Most experts recommend having 7 to 8 times your annual income saved by age 60, but the median American savings fall dramatically short of that target, creating a gap that requires urgent action.

What are the 2026 catch-up contribution limits for 401(k) and IRA?

In 2026, savers aged 50 and older can contribute an extra $7,500 to a 401(k) and $1,000 more to an IRA above the regular annual limit.

Is the 4% rule still safe for retirement withdrawals in 2026?

The 4% withdrawal rule remains a widely used starting point, but market volatility and longer lifespans mean you should revisit it regularly and adjust based on your actual portfolio and spending needs.

Should I delay Social Security past 67?

Delaying Social Security beyond your full retirement age adds roughly 8% per year in benefits up to age 70, making it one of the most powerful income-boosting strategies available if your health allows it.

Recommended

Comments