How Life Insurance Works: A Clear Guide for Family Security

- JF Strawderman

- Apr 22

- 9 min read

TL;DR:

Life insurance payouts are highly reliable, with a claim payout rate of 98.1%.

Term and permanent policies serve different needs, with term being affordable and temporary.

Proper policy management, honesty, and updates ensure beneficiaries receive benefits smoothly.

Few families realize just how reliably life insurance pays out. US insurers paid $28.5B in individual death benefits in 2022 alone, with an average payout between $182,000 and $195,000. The claim denial rate? Just 1.9%. That means when a policy is in place and maintained correctly, the money almost always reaches your family. Yet millions of Americans remain uninsured or underinsured because the process feels complicated or confusing. This guide breaks down exactly how life insurance works, what types exist, how payouts happen, what affects your premiums, and how to avoid the mistakes that could leave your family short.

Table of Contents

Key Takeaways

Point | Details |

High payout reliability | Life insurance claims are approved nearly 98 percent of the time, creating dependable security for families. |

Know your policy type | Choosing between term and permanent coverage depends on your needs and long-term goals. |

Key factors affect costs | Premiums and approval are mainly based on age, health, and coverage amount. |

Avoid common mistakes | Updating beneficiaries and keeping your policy active helps loved ones receive full benefits. |

Make it part of your plan | A well-chosen life insurance policy is a cornerstone of effective family financial planning. |

The basics: What is life insurance?

Life insurance is a legal contract between you (the policyholder) and an insurance company (the insurer). You agree to pay a regular amount called a premium, and in return, the insurer agrees to pay a set amount of money called the death benefit to your chosen beneficiary when you pass away. It is as straightforward as that at its core.

Your beneficiary can be a spouse, child, sibling, or even a trust or business partner. They receive the payout tax-free in most cases, and they can use the funds for almost any purpose. Common uses include:

Replacing lost household income so a surviving spouse can pay bills

Paying off a mortgage or car loan

Covering funeral and burial costs, which average over $7,000 nationally

Funding a child’s college education

Leaving a financial legacy or charitable gift

The industry as a whole demonstrates just how vital this protection is. US insurers paid $28.5B in individual benefits in 2022, showing that policies genuinely do what they promise. Understanding why life insurance matters for your specific family situation is the first step toward making an informed decision.

Reviewing top life insurance claims data can also show you how other families have used their coverage, giving you a clearer sense of real-world impact.

Pro Tip: Review your policy at least once a year. Marriage, divorce, a new baby, or a job change can all shift how much coverage you need and who should be your beneficiary.

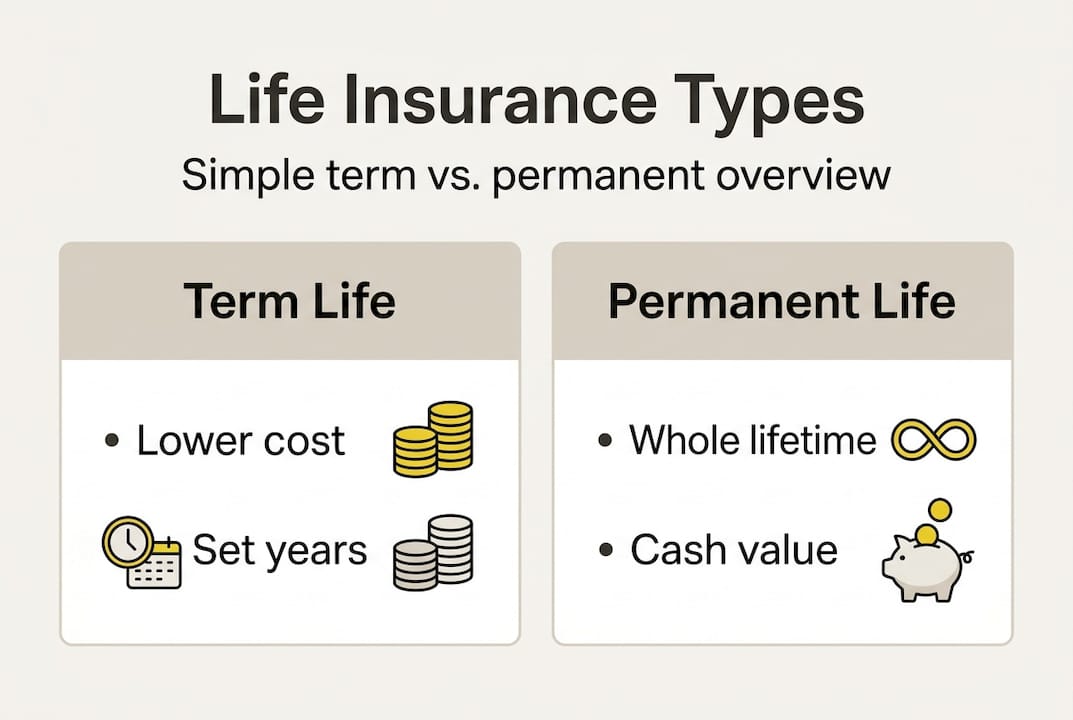

Types of life insurance: Term vs. permanent

Not all life insurance is the same, and picking the wrong type can mean paying too much or not being covered when it counts. The two main categories are term life insurance and permanent life insurance.

Term life insurance covers you for a set period, typically 10, 20, or 30 years. It is generally affordable and straightforward. If you pass away during the term, the insurer pays the death benefit. If you outlive the term, coverage ends with no payout. There is no savings or investment component.

Permanent life insurance (which includes whole life and universal life) covers you for your entire lifetime as long as premiums are paid. It also builds cash value over time, a feature that acts like a savings account you can borrow against. It costs significantly more than term policies.

Feature | Term Life | Permanent Life |

Cost | Lower premiums | Higher premiums |

Duration | Fixed period | Lifetime |

Cash value | None | Yes |

Best for | Income replacement | Legacy and wealth |

Typical buyer | Young families | High-net-worth individuals |

Three questions to guide your choice:

How long do you need coverage? If it is only until your kids are grown, term may be enough.

Do you want a savings component built into your policy?

What is your monthly budget for premiums?

For most working families, term life insurance explained simply is the most practical starting point. Experts often recommend the “buy term and invest the difference” strategy, meaning you purchase affordable term coverage and put the premium savings into other investments. That said, permanent coverage options suit high-net-worth individuals who want tax advantages and legacy planning.

Pro Tip: Young parents often do best with a 20 or 30-year term policy that lasts until children are financially independent. As your wealth grows, you can explore permanent options.

How claims work: From filing to payout

Understanding the claim process removes a lot of anxiety for families. Here is what typically happens after a loved one passes away:

The beneficiary contacts the insurance company to notify them of the death.

The insurer provides a claim form and requests a certified copy of the death certificate.

Additional documents may be requested, such as the original policy paperwork or medical records.

The insurer reviews the claim and verifies the policy is in good standing.

Once approved, payment is issued, usually within 30 to 60 days.

“The denial rate for life insurance claims is only around 1.9%, meaning the vast majority of families who file receive the full benefit they were promised.”

Here is a look at how claim outcomes typically break down:

Outcome | Percentage |

Claims paid in full | ~98.1% |

Claims denied | ~1.9% |

Top cause: cancer | 32% of claims |

Top cause: heart disease | 24% of claims |

The top reasons claims get denied are misrepresentation on the application, policy lapse due to missed premiums, or filing during an exclusion period. Protecting loved ones from these outcomes means keeping your policy active and being honest when you apply.

To set your family up for a smooth process, keep a copy of your policy in a safe and accessible place. Let your beneficiary know where it is, who the insurer is, and how to file. Small steps now can prevent big delays during an already difficult time. You can also explore common claim outcomes to better understand what beneficiaries experience.

What affects your premiums and approval?

Insurers do not set prices randomly. They use a process called underwriting to assess your risk level and decide what you will pay. The lower your risk, the lower your premium. Several factors shape this calculation.

Factors that affect your premium:

Age: The younger you are when you apply, the less you pay. Rates increase with every year you wait.

Health status: Chronic conditions like diabetes or high blood pressure raise your rates. Serious illnesses can lead to denial.

Smoking status: Smokers typically pay two to three times more than nonsmokers for the same coverage.

Occupation: High-risk jobs like construction or commercial fishing can raise premiums.

Lifestyle: Activities like skydiving or motorcycle racing are viewed as added risk.

Family history: A history of heart disease or cancer in close relatives is considered.

It is worth noting that cancer accounts for 32% of life insurance claims and heart disease accounts for 24%. These statistics reinforce why insurers pay close attention to your health history, and why understanding impact of health on insurance eligibility matters so much before you apply.

You can improve your approval odds by applying while you are young and healthy, quitting smoking at least 12 months before applying, and being fully transparent on your application. Nondisclosure, meaning leaving out health information, is the most common reason claims are later contested. Your health history and approval chances are closely tied, so honesty protects both you and your family in the long run.

Avoiding common mistakes and making life insurance work for you

Even families with good intentions make avoidable mistakes that reduce or eliminate their benefit. Knowing what to watch out for keeps your coverage strong.

Common policyholder mistakes:

Letting the policy lapse by missing premium payments

Naming outdated beneficiaries (such as an ex-spouse or a deceased parent)

Underestimating how much coverage you actually need

Not telling your beneficiary the policy exists

Choosing the cheapest option without reading exclusions

Forgetting to update the policy after major life events

The denial rate is only 1.9% when all requirements are met, which means most claim problems are preventable. The real risk is not that the insurer will refuse to pay. The real risk is that the policy was not set up correctly in the first place.

Coordinating life insurance with your broader financial plan matters too. Think of it as one part of a larger strategy. You might be comparing policies alongside retirement accounts, emergency savings, and disability coverage. Each piece plays a different role, but together they protect your family from multiple directions. Looking at retirement planning and insurance together gives you a fuller picture of your financial security.

Pro Tip: Tell your beneficiary exactly where the policy documents are stored and include the insurer’s contact number. One conversation now could save them weeks of stress later.

A better way to think about life insurance

Most conversations about life insurance center on worst-case scenarios. Death. Loss. Grief. That framing is not wrong, but it is incomplete, and it keeps many people from acting.

Here is a different angle worth considering: life insurance is also a tool for financial leverage and peace of mind while you are still alive. Knowing your family would be taken care of frees you to take career risks, start a business, or pursue goals you might otherwise avoid. That is not morbid. That is empowerment.

We have seen clients who put off getting covered for years because they associated the process with confronting their own mortality. Once they went through it, almost universally they described the feeling as relief, not dread. The act of planning is itself a form of control in an unpredictable world.

Permanent policies with cash value also contribute to life insurance for long-term wealth building in ways that pure term coverage cannot. The key is viewing your policy not as a static document you file away, but as a living part of your financial strategy that grows and adjusts with you.

Take your next step toward peace of mind

Now that you have a clear picture of how life insurance works, the next step is finding coverage that fits your specific situation. Reading about policies is valuable, but a real conversation with a knowledgeable advisor makes all the difference when it comes to protecting your family.

At Strawderman Financial, we specialize in helping families across the United States find life insurance solutions that match their budget and goals. Whether you are starting fresh or reviewing an existing policy, our team offers free consultations to walk you through your options with no pressure. We also offer comprehensive planning support so your insurance fits naturally into your overall financial picture. Ready to protect what matters most? Speak with a professional at Strawderman Financial today and take that first confident step forward.

Frequently asked questions

How long does it take for a life insurance claim to pay out?

Most claims are paid within 30 to 60 days once all documents are submitted and the policy is confirmed to be in good standing. Delays usually stem from missing paperwork, not insurer reluctance, since US insurers paid $28.5B in benefits in 2022 alone.

What can cause a life insurance claim to be denied?

The most common reasons include material misrepresentation on the application, a lapsed policy due to unpaid premiums, or a claim filed during an exclusion period. With a denial rate of ~1.9%, most claims are approved when the policy is kept in good standing.

Is life insurance taxable to beneficiaries?

In most cases, life insurance death benefits are received income tax-free by beneficiaries. However, very large estates may face estate tax considerations depending on how the policy is structured.

Can I have more than one life insurance policy?

Yes, you can hold multiple life insurance policies simultaneously. Insurers simply want to confirm that the total coverage amount is reasonable relative to your income and insurable interest.

What’s the difference between a death benefit and cash value?

The death benefit is the lump sum paid to your beneficiary when you pass away. Cash value is a separate savings component found only in permanent policies that you can borrow against or withdraw while you are still alive.

Recommended

Comments