How to Assess Critical Illness Insurance Needs: 2026 Guide

- JF Strawderman

- Apr 20

- 8 min read

TL;DR:

Critical illness insurance provides tax-free lump sums to cover living expenses during serious health conditions.

Assessing personal risks and detailed expenses helps determine the appropriate coverage amount.

Proper planning involves understanding policy options, avoiding common mistakes, and integrating coverage into broader financial strategies.

A cancer diagnosis, a stroke, or a sudden heart attack doesn’t just affect your health. It can drain your savings account within months. Medical bills pile up fast, but so do everyday costs like mortgage payments, groceries, and childcare that don’t pause while you recover. Many families discover too late that their regular health insurance covers hospital bills but leaves a massive gap in living expenses and lost income. Critical illness insurance exists to fill that gap, paying you a lump sum directly when you need it most. This guide walks you through a clear, step-by-step process to figure out exactly how much coverage your family needs.

Table of Contents

Key Takeaways

Point | Details |

Know your risks | Personal and family medical history directly impact your coverage needs and cost. |

Calculate actual expenses | Tally medical and living expenses, then subtract existing protection before choosing coverage. |

Compare policy options | Not all critical illness plans are alike—review costs, features, and eligibility rules carefully. |

Avoid common pitfalls | Double-check your assessment each year and don’t just rely on employer insurance. |

Understanding critical illness insurance

Not everyone is familiar with how critical illness insurance works, and that’s where most people go wrong before they even start shopping. This type of policy pays you a tax-free lump sum if you’re diagnosed with a serious, covered condition. You use that money however you choose, whether that’s paying your rent, covering experimental treatment, or keeping your business running while you’re out of work.

Critical illness policies typically cover conditions like heart disease, cancer, or stroke. Beyond those three, many plans also include:

Kidney failure

Major organ transplants

Paralysis

Coronary artery bypass surgery

Coma or traumatic brain injury

This is very different from your standard health plan. Your types of health insurance coverage pays providers directly for medical services rendered. Critical illness insurance pays you, giving you control over how the money is spent. It’s also different from life insurance, which only pays out after death.

“Critical illness insurance is not a replacement for health coverage. It’s a financial safety net that protects your income and lifestyle when a major diagnosis forces you off your feet for weeks or months.”

One common misconception is that these policies cover every health setback. They don’t. Coverage is limited to specifically defined conditions listed in your policy contract. Familiarizing yourself with key insurance terms before signing anything will help you read the fine print with confidence. When you file a claim, you typically provide a confirmed diagnosis from a licensed physician, and the insurer pays out a predetermined benefit amount, usually within 30 days.

Identify your personal risk factors

Understanding what’s covered is the first step. Next, you need to examine your specific health risk profile before you can put a dollar figure on your coverage needs.

Personal risk factors including family medical history, age, and lifestyle influence coverage needs and premium costs significantly. Here’s what to look at honestly:

Age: The older you are, the higher your statistical risk and your premium

Family history: A parent or sibling diagnosed with heart disease or cancer before age 60 is a major red flag

Lifestyle habits: Smoking, high BMI, and sedentary behavior all raise risk considerably

Existing health conditions: Diabetes, hypertension, or high cholesterol can affect your eligibility and cost

Occupation: High-stress or physically demanding jobs can factor into underwriting decisions

The impact of pre-existing conditions on your policy options is real. Some insurers exclude conditions you already have, while others offer coverage with adjusted premiums. This is why it’s important to apply sooner rather than later, before your health history gets more complex.

Pro Tip: Pull your family’s medical records going back two generations if possible. Knowing your grandfather had a stroke at 58 is exactly the kind of information that should shape your coverage amount and urgency.

To gather what you need, write down every diagnosed condition in your immediate family, your current medications, your last three years of lab results, and any lifestyle habits your doctor has flagged. This preparation will also speed up your application process considerably and help you think about protecting your family with the right amount of coverage rather than guessing.

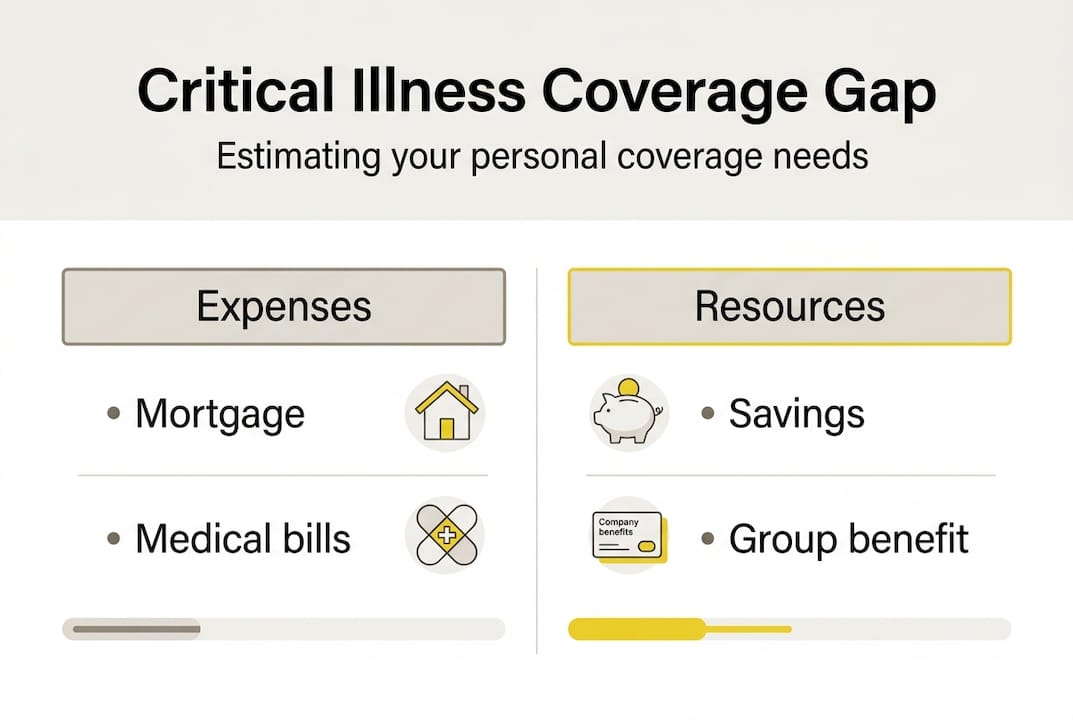

Calculate your coverage needs: a step-by-step process

After identifying your risks, it’s time to put real numbers to your potential needs. This process doesn’t require a financial advisor, but it does require honesty about your expenses and obligations.

Follow this four-step method to arrive at a realistic coverage figure:

Inventory your risks and family history to determine which conditions you’re most likely to face

List all monthly expenses and debts, including mortgage or rent, car payments, utilities, food, and childcare

Estimate your income gap, meaning how many months of income would be lost if you couldn’t work during treatment and recovery

Subtract your savings and existing insurance benefits from your total estimated need to find your true coverage gap

Here’s a sample breakdown to make this concrete:

Expense category | Monthly cost | 12-month total |

Mortgage/rent | $1,800 | $21,600 |

Car and transportation | $550 | $6,600 |

Utilities and groceries | $700 | $8,400 |

Childcare or school fees | $900 | $10,800 |

Out-of-pocket medical | $500 | $6,000 |

Total estimated need | $4,450 | $53,400 |

If you have $15,000 in savings and your employer provides a $10,000 group benefit, your coverage gap is roughly $28,400. That’s the minimum lump sum you should target when comparing insurance policies.

Pro Tip: Don’t forget to factor in debt payoff. If a serious illness would make your credit card or personal loan payments impossible to maintain, add those balances to your coverage calculation.

Understanding whether group vs individual plans better fit your situation also shapes this number. Group plans often have lower benefit caps, which means individual coverage may be necessary to meet your real-world needs.

Breakdown of costs and policy options

Having calculated your prospective coverage, you’re ready to compare real-world policy options and understand the true costs involved.

Premiums vary from $20 to $100 or more per month based on age and benefit level. The biggest cost drivers include:

Age at enrollment: A 35-year-old pays significantly less than a 55-year-old for the same benefit

Coverage amount: A $50,000 benefit costs far less than a $150,000 policy

Health status: Smokers and those with chronic conditions pay higher premiums

Number of conditions covered: Broader coverage means higher cost

Here’s a general comparison of policy structures available in 2026:

Policy type | Benefit range | Best for | Avg. monthly cost |

Individual standalone | $10,000 to $500,000 | Self-employed, high earners | $30 to $120 |

Group plan (employer) | $5,000 to $50,000 | Employees needing basic coverage | $10 to $40 |

Rider on life policy | $10,000 to $100,000 | Those with existing life insurance | $15 to $60 |

When thinking about why buy life insurance alongside critical illness coverage, the case for a rider becomes clear. You can often add critical illness benefits to an existing policy at a fraction of the standalone cost.

Stat to know: A single cancer diagnosis costs the average American family over $42,000 in out-of-pocket expenses during the first year alone, far exceeding what most emergency funds can absorb.

When choosing health insurance, always factor in how a critical illness plan would work alongside your deductible and out-of-pocket maximum. The two work together, not in competition.

Common mistakes and how to double-check your needs

Before finalizing your protection, make sure to avoid common mistakes and recheck your numbers carefully.

Many people underestimate future costs or rely solely on employer coverage, and families often neglect to revisit needs as circumstances change. Here’s how to avoid that trap:

Don’t assume health insurance covers everything. It covers medical bills, not your mortgage or lost wages.

Avoid relying entirely on employer benefits. Most group plans cap benefits too low to cover a full recovery period.

Don’t forget debt. Car loans, student debt, and credit cards don’t pause because you’re ill.

Revisit your needs annually. A new baby, a promotion, or a new mortgage changes your coverage math completely.

Get a second opinion on your coverage amount. An agent review can catch gaps you missed.

“The most dangerous assumption in insurance planning is thinking what worked last year still works today. Life changes fast, and your coverage should keep up.”

Use this quick double-check before you sign anything: confirm your listed expenses are current, verify your savings figures are accurate, and make sure you’ve accounted for all income sources that would be disrupted by an illness, not just your primary paycheck.

The insurance blog and resources at Strawderman Financial offer updated tools and guidance that can help you review your numbers at any stage.

A smarter way to approach critical illness insurance

Now that we’ve broken down the process, here’s an experienced perspective on what really matters and what most people miss entirely.

Many families make the mistake of buying the largest lump sum they can afford without thinking about whether that amount actually matches their lifestyle. A single person renting an apartment in Ohio has very different needs than a two-income household with a mortgage and three kids in Georgia. Bigger is not always smarter.

The real value of a well-designed critical illness policy isn’t the dollar amount alone. It’s the flexibility of how that money can be used. Riders that add return-of-premium features or waiver-of-premium benefits during a claim can make a mid-range policy far more valuable than a high-dollar bare-bones plan.

We also believe that critical illness insurance should never exist in isolation. It belongs inside a broader retirement strategy and financial plan, reviewed every year the same way you’d review your retirement contributions or your tax strategy. Treat it as a living document, not a one-time purchase.

Ready to protect your finances? Next steps

With your assessment in hand, you’re ready to take confident action toward real financial protection.

At Strawderman Financial, we work with individuals and families across the U.S. to build personalized coverage strategies that account for your exact income, debts, health profile, and goals. There is no one-size-fits-all plan here.

Our agents specialize in matching families with the right mix of life insurance options and health insurance solutions so your critical illness coverage works alongside everything else you have in place. We offer free consultations, no pressure, and straightforward guidance. Visit Strawderman Financial today to schedule your free coverage review and stop leaving your family’s financial security to chance.

Frequently asked questions

What conditions does critical illness insurance usually cover?

Most policies cover heart attack, cancer, stroke and may also include organ failure, major organ transplants, or serious surgeries depending on the plan.

How much will my premium cost for critical illness insurance?

Premiums typically range from $20 to over $100 per month, with your age, chosen benefit amount, and current health status being the primary factors.

What’s the most common mistake when assessing critical illness needs?

Most people underestimate total costs by focusing only on medical bills and forgetting that everyday living expenses continue throughout a long recovery period.

Does my employer’s insurance cover all my critical illness needs?

Employer coverage alone rarely provides enough protection, and adding a supplemental individual policy is often the most practical way to close that gap.

Recommended

Comments