Disability insurance explained: Protect your income and future

- JF Strawderman

- Apr 25

- 8 min read

TL;DR:

Most disability claims stem from illnesses like cancer and mental health, not accidents.

Short-term policies cover immediate recovery needs, while long-term plans provide ongoing protection.

Disability insurance is essential for all working adults, with a focus on income replacement and proper claim management.

Most people picture a disability as something dramatic, a workplace accident or a sudden fall. The reality is far more sobering. 1 in 4 of today’s 20-year-olds will become disabled before they reach retirement age, and the culprit is usually not an accident at all. It is cancer, heart disease, depression, or a chronic back condition. Disability insurance exists to replace your income when illness or injury stops you from working, and understanding how it works could be the most important financial decision you make this decade. This article walks you through what disability insurance covers, how the two main types differ, how claims are processed, and how to pick the right policy for your situation.

Table of Contents

Key Takeaways

Point | Details |

Most claims from illness | Disability insurance claims are mostly from common illnesses, not accidents. |

Income protection is essential | Your income is at risk—disability insurance ensures you have financial support if you can’t work. |

Short-term vs long-term | Short-term covers months; long-term can replace income for years and up to retirement age. |

Approval rates vary | Private long-term disability policies approve most claims, but government SSDI approval is lower. |

Choose tailored coverage | Consider your personal needs and risk factors when selecting disability insurance. |

The basics: What disability insurance covers

Disability insurance is simply a policy that replaces a portion of your paycheck if you cannot work due to illness or injury. Most policies replace between 60% and 80% of your pre-disability income, paid as a monthly benefit. That income keeps your rent paid, your groceries stocked, and your family financially stable while you recover.

Here is where most people get surprised. Over 90% of disability claims come from illnesses, not accidents. Conditions like musculoskeletal disorders, mental health diagnoses, and cancer are far more likely to sideline you than a workplace injury. That changes the conversation completely about who needs this coverage.

There are three key definitions you should know before choosing a policy:

Total disability: You cannot perform any duties of your occupation at all.

Partial disability: You can work in a reduced capacity but earn less income than before.

Residual disability: Similar to partial, this pays a proportional benefit based on your income loss, which is useful for gradual recoveries.

“The definition of disability in your policy is arguably the most important clause to read. An ‘own-occupation’ definition means you qualify if you cannot do YOUR specific job, while ‘any-occupation’ means you must be unable to do virtually any work.”

Pro Tip: Always ask for an own-occupation definition if you work in a specialized field like medicine, law, or skilled trades. It offers far stronger protection.

So who needs disability insurance? Honestly, any working adult who could not maintain their lifestyle without their paycheck. Understanding how your health and finances intersect is a good starting point, and our smart coverage guide can help you see the bigger picture of protection.

Short-term vs long-term disability: Key differences

Understanding the two main types of disability insurance helps clarify your choices. They are designed to work differently, and in many cases, together.

Short-term disability (STD) kicks in quickly. The elimination period (the waiting time before benefits begin) is typically zero to 14 days. Coverage usually lasts three to six months, though some policies extend to 12 months. Think of STD as your bridge: it covers the gap right after an illness or surgery.

Long-term disability (LTD) takes over where short-term leaves off. The elimination period is usually around 90 days, so it is designed to start after your STD coverage ends. LTD can pay benefits for years or until age 65, depending on your policy terms.

Here is a quick comparison:

Feature | Short-term disability | Long-term disability |

Waiting period | 0 to 14 days | 60 to 90 days |

Benefit duration | Up to 12 months | 2 years to age 65 |

Coverage amount | 60% to 100% of income | 50% to 80% of income |

Best for | Recovery from surgery, illness | Serious conditions, chronic illness |

Cost | Lower premiums | Higher premiums |

Here is how a smart layered strategy works:

Emergency fund: Covers the first week or two before STD activates.

Short-term disability: Replaces income during the first few months.

Long-term disability: Provides sustained protection for extended disabilities.

Savings and investments: Supplement benefits to close any income gap.

This layered approach is a core part of solid financial planning. If you want to see how disability coverage fits alongside other policies, our insurance policy comparison resource lays it out clearly.

How claims work: Approval, denial, and common causes

Once you choose coverage, it is crucial to understand what happens when you file a claim. The process varies depending on whether you have private insurance or are applying for government benefits.

Here is what the data actually shows:

Insurance type | Approval rate | Notes |

Private LTD | ~85% | Strong approval for documented claims |

Private STD | ~85% | Similar to LTD |

SSDI (initial) | ~35% | Social Security Disability; most denied at first |

SSDI (appeals) | Higher | Many approvals happen at the appeal stage |

Private disability insurance has a denial rate of about 15%, which means the large majority of well-documented claims get paid. SSDI (Social Security Disability Insurance), the government program, is far stricter with an initial approval rate of just 35%.

The top causes of claims include musculoskeletal disorders like back pain, mental health conditions like depression and anxiety, and cancer. These are not rare events. They are the everyday health challenges millions of Americans face.

Here are key steps to strengthen your claim:

Keep thorough medical records from the day your condition begins.

Follow your doctor’s treatment plan consistently and document all appointments.

Notify your insurer promptly as soon as you know you need to file.

Understand your policy’s definitions so you know exactly what you are claiming.

Get professional guidance when navigating complex claims.

Pro Tip: Do not wait until you are certain about your diagnosis to contact your insurer. Early communication can prevent procedural delays.

Managing your wealth accumulation strategies while navigating a disability is incredibly difficult. Reading through our disability insurance blog can give you practical next steps. And if you have pre-existing conditions, understanding how they affect your claim eligibility is essential before you buy.

Choosing the right disability insurance for you

With claim process knowledge, you are ready to identify the best disability insurance for your needs. The right policy is not always the most expensive one. It is the one that fits your income, your job, and your life situation.

Start by working through these core factors:

Income replacement needs: Calculate how much monthly income you would need to cover your essential expenses if you stopped working tomorrow.

Elimination period: Can you survive 30, 60, or 90 days without income? The longer you can wait, the lower your premium.

Benefit period: A policy that pays to age 65 costs more but offers far more security. Remember, the average LTD claim lasts 2.5 to 3.5 years, so short coverage windows can leave you exposed.

Own-occupation vs any-occupation definition: Already covered above, but worth repeating. Own-occupation is almost always the better choice for professionals.

Residual or partial disability benefits: If your condition limits but does not eliminate your ability to work, residual benefits pay a proportional amount. This is hugely valuable for gradual recoveries.

You also need to decide between group and individual coverage:

Group coverage (offered through an employer) is convenient and often cheaper, but benefits are typically taxable and the policy may not follow you if you change jobs.

Individual coverage costs more upfront but is portable, often tax-free if you pay premiums yourself, and customizable.

Pro Tip: If your employer offers group disability coverage, check whether you can supplement it with an individual policy to close any income gaps.

Reviewing group vs individual health plans can help you understand how coverage structures differ. Our breakdown of smart insurance picks also gives you a broader view of how disability coverage fits within your overall protection strategy.

The real risk: Why disability insurance isn’t just “a safety net”

Let’s pause for an honest look at why disability insurance matters more than most people think.

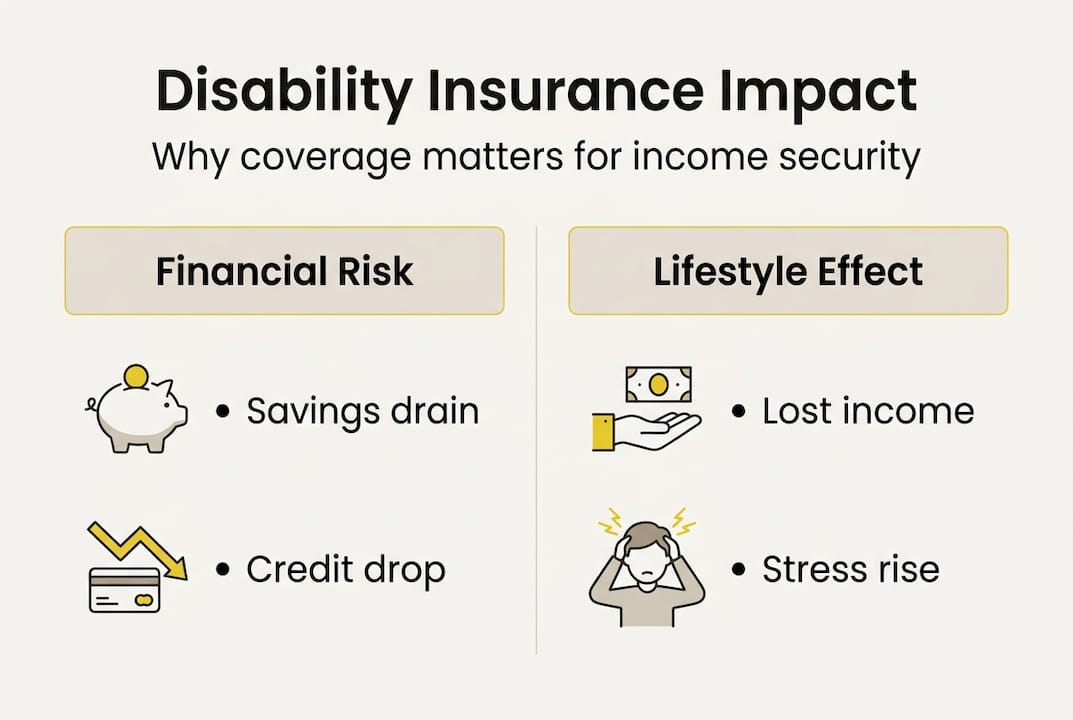

Here is the uncomfortable truth. Most people do not buy disability insurance because they picture themselves in an accident. They figure they are careful, they drive safely, they do not work in a dangerous environment. And they are probably right about the accident part. But that thinking completely misses the actual risk.

Over 90% of disability claims come from illnesses, including depression, anxiety, and chronic pain. You do not get to opt out of illness by being careful. And with 1 in 4 young adults facing disability before retirement, this is not a rare edge case. It is a mainstream financial risk.

The financial consequences of going uninsured are severe. Without income, savings evaporate within months. Credit gets damaged. Retirement accounts get raided early. Families face impossible choices. Disability insurance is not a luxury product for cautious people. It is essential income protection, the same way you would not drive without car insurance even if you consider yourself a careful driver.

Treat disability coverage as a core part of your financial foundation, not an optional add-on.

Protect your income with expert help

Understanding disability insurance is the first step. Putting the right plan in place is what actually protects you.

At Strawderman Financial, we help individuals and families across the United States find coverage that fits their real lives, not just a generic policy off a shelf. Whether you are looking at life insurance options, health insurance plans, or building a broader retirement planning strategy, our agents provide personalized guidance with no pressure. Schedule a free consultation and let us help you close the gaps before a disability closes them for you.

Frequently asked questions

Who needs disability insurance?

Anyone who depends on their paycheck to cover living expenses should consider disability insurance, especially since over 90% of claims come from illnesses rather than accidents.

How long does disability insurance pay benefits?

Short-term disability usually pays for up to 12 months, while long-term disability policies can pay benefits all the way until age 65, depending on your policy terms.

What are the most common reasons disability insurance claims are filed?

Musculoskeletal disorders and mental health conditions are the leading causes of disability claims, far outpacing workplace accidents in frequency.

Is group disability insurance enough for most people?

Group coverage is a helpful starting point, but it often covers only a portion of your income and may not follow you between jobs. Partial disabilities are common, and individual policies tend to offer more complete protection.

How likely am I to qualify for disability insurance benefits?

Private LTD policies have an approval rate of about 85% for documented claims, while SSDI initial approval sits around 35%, making private coverage a much more reliable option for most working adults.

Recommended

Comments