How to Choose Health Insurance: Smart Steps for 2026

- JF Strawderman

- Apr 12

- 8 min read

TL;DR:

Carefully assess your healthcare needs and usage patterns before selecting a plan.

Total annual cost analysis is more important than just comparing premiums.

Verify provider networks and formulary coverage to prevent unexpected expenses.

Imagine opening your mailbox to find that your health insurance premium jumped by double digits this year, and you have no idea whether your plan still covers your doctor, your prescriptions, or that specialist you rely on. That scenario is playing out for millions of Americans in 2026. Marketplace premiums are rising, subsidies are shifting, and the stakes for picking the wrong plan have never been higher. Whether you are an individual, a family, or someone planning an early retirement, this guide breaks down the exact steps to compare, evaluate, and choose the right health insurance with confidence.

Table of Contents

Key Takeaways

Point | Details |

Focus on total costs | Don’t just compare premiums—review deductibles, copays, and out-of-pocket limits to find your best value. |

Check networks and drugs | Always confirm your providers and medications are in-network before enrolling in a plan. |

Account for 2026 changes | Be aware of subsidy cutbacks and premium hikes for 2026 that may impact your best option. |

Use comparison tools | Leverage online calculators and plan directories to filter and compare your best-fit plans. |

Understanding your health insurance needs

Before you compare a single plan, you need a clear picture of what you actually use. Think of this step as building your personal healthcare profile. Without it, you are essentially shopping blind, and that is how people end up with low premiums but massive bills.

Start by estimating how often you visit doctors, fill prescriptions, or use specialist care in a typical year. Then think about what is coming: Are you planning a pregnancy? Do you have a chronic condition like diabetes or high blood pressure? Are you retiring in the next year or two and losing employer coverage? Each of these factors changes which plan type and benefit structure makes the most sense for you.

Knowing what smart health coverage means before you shop helps you filter out plans that look attractive on paper but leave critical gaps. And if you have a pre-existing condition, understanding the impact of pre-existing conditions on your coverage options is essential before you commit to any plan.

Here is a quick needs checklist to complete before comparing plans:

Prescription drugs: List all current medications and dosages

Regular providers: Note your primary care doctor, specialists, and preferred hospital

Planned procedures: Include any surgeries, screenings, or treatments scheduled

Mental health services: Confirm if therapy or psychiatric care is needed

Maternity or pediatric care: Flag if you are expecting or have young children

Chronic condition management: Identify ongoing care needs that require frequent visits

“When choosing a health plan, prioritize total cost over premiums alone to get the best value.” This means looking beyond the monthly bill and thinking about what you will actually spend across the whole year.

Pro Tip: Write your needs list before visiting any comparison website. Families that do this tend to choose plans that actually fit their lives, not just their budgets.

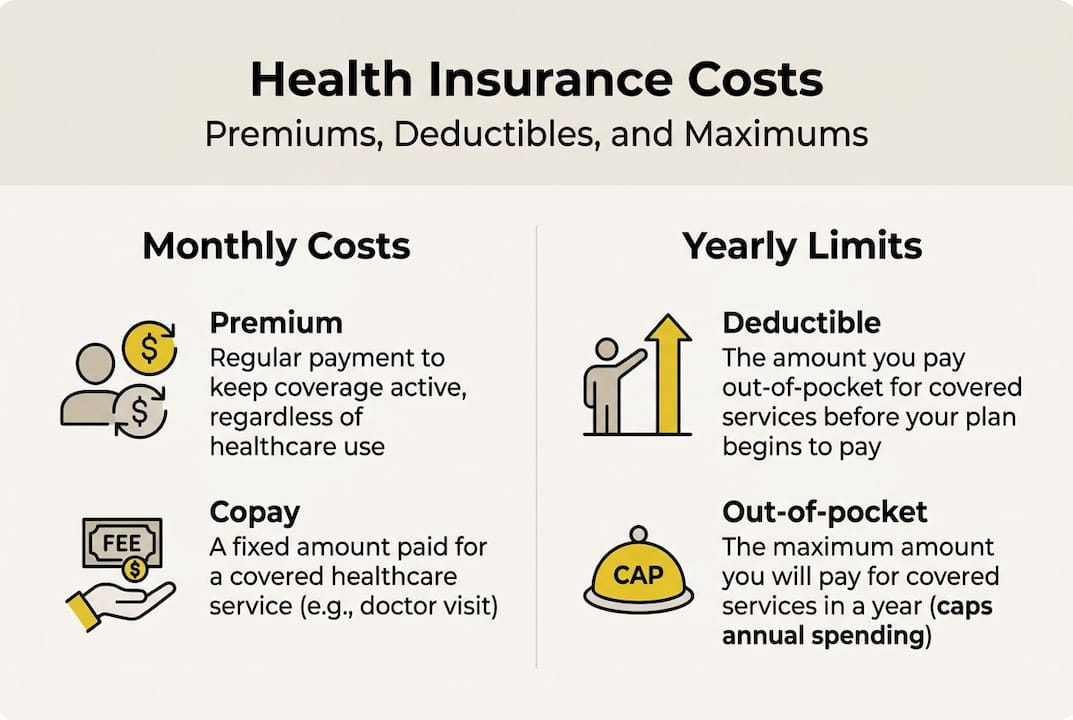

Comparing costs: premiums, deductibles, and out-of-pocket expenses

Now that you have evaluated your needs, let’s look at the most important cost factors and how to analyze them side by side. Health insurance pricing has multiple layers, and each one affects your real annual cost.

Premium is the monthly amount you pay regardless of whether you use care. Deductible is what you pay out of pocket before your insurer starts covering most services. Copay is a flat fee per visit or prescription. Coinsurance is your percentage share of costs after meeting your deductible. The out-of-pocket maximum is the most you will ever pay in a single year, after which insurance covers 100%.

Here is a simplified comparison of how these costs interact across common plan tiers:

Plan tier | Avg. monthly premium | Avg. deductible | Out-of-pocket max |

Bronze | Lower | $7,000+ | $9,450 |

Silver | Moderate | $3,500–$5,000 | $9,450 |

Gold | Higher | $1,000–$2,500 | $9,450 |

Platinum | Highest | $0–$500 | $9,450 |

In 2026, average ACA marketplace premiums have increased in most states, but premium tax credits offset costs for many enrollees. The key insight: total cost, not just premiums is what determines whether a plan is truly affordable for your situation.

Here is a step-by-step approach to estimate your real annual cost:

Multiply your monthly premium by 12 to get your yearly premium total

Add your expected out-of-pocket spending based on typical usage

Factor in your deductible if you anticipate hitting it

Add copays and coinsurance for specialist visits or prescriptions

Compare this total across your shortlisted plans, not just the monthly rate

Families dealing with insurance and chronic conditions often find that a Gold plan with higher premiums costs less overall than a Bronze plan with a massive deductible. Understanding major health insurance types also helps you match cost structure to your usage pattern.

Pro Tip: Run a “worst-case” scenario. Assume you hit your out-of-pocket maximum. Which plan costs less in that situation? That is often the smarter choice for families with unpredictable health needs.

Evaluating networks, drug coverage, and essential benefits

Once you have clarified the dollar figures, it is essential to see what providers and services each plan option truly offers. A plan with a great premium means nothing if your doctor is not in the network.

In-network providers have agreed to negotiated rates with your insurer, which keeps your costs significantly lower. Going out of network can mean paying full price or being denied coverage entirely, depending on your plan type. This is one of the most common and costly surprises people face after enrolling.

Before you finalize any plan, check provider network and drug formulary details carefully. Most insurers publish online directories where you can search by doctor name, specialty, or hospital. Do the same for your prescriptions using the plan’s drug formulary list.

Here is a comparison of how different plan types handle networks:

Plan type | Network flexibility | Referrals needed | Out-of-network coverage |

HMO | Narrow | Yes | Usually none |

PPO | Broad | No | Yes, at higher cost |

EPO | Moderate | No | Usually none |

HDHP | Varies | Varies | Varies |

Beyond networks, confirm that each plan includes these essential health benefits:

Preventive and wellness services

Emergency services

Mental health and substance use treatment

Prescription drug coverage

Maternity and newborn care

Pediatric services, including dental and vision for children

Rehabilitative and habilitative services

Understanding plan types and networks helps you match the right structure to your family’s care patterns. A family that sees multiple specialists regularly will almost always benefit from a PPO’s flexibility, even at a higher cost.

Making your choice: deciding factors and application tips

With a shortlist in hand, you are ready to choose and enroll in your best health insurance option. This final stage is where many people make avoidable mistakes, especially with the changes that took effect in 2026.

Follow these steps to finalize your decision:

Gather all plan documents, including Summary of Benefits and Coverage sheets

Filter your shortlist by must-have providers and medications

Calculate total annual cost for each plan using the method from the previous section

Verify network and formulary details for your specific doctors and drugs

Apply through Healthcare.gov, your state marketplace, or a licensed agent

Set a calendar reminder for open enrollment deadlines

A major 2026 consideration: ACA premium increases and subsidy changes have created new financial traps, especially for households earning above 400% of the federal poverty level. The enhanced subsidies that helped many families in recent years have been restructured, and missing these details can mean a significant jump in your net premium.

Statistic callout: According to 2026 Marketplace fact sheet data, the average after-credit premium for enrollees receiving premium tax credits remains relatively affordable, but eligibility thresholds have shifted, making it critical to check your specific income bracket before assuming you qualify.

For early retirees, this step is especially urgent. If you retire before age 65, you face a gap before Medicare eligibility kicks in. Bridging that gap with the right marketplace plan requires careful attention to income-based subsidies, network continuity, and premium stability. Using insurance comparison tools designed for retirement transitions can save you thousands. You can also browse recent articles on 2026 updates to stay current on policy changes.

Pro Tip: If your income is close to a subsidy threshold, even a small change in reported income can shift your premium tax credit significantly. Talk to a licensed agent before finalizing your application.

A smarter way to choose health insurance in 2026: what most guides miss

Here is the part most step-by-step guides skip entirely: the standard advice to “compare plans and pick the best one” assumes you have perfect information and unlimited time. Real families do not.

The most overlooked mistake is fixating on the monthly premium. We see it constantly. Someone picks a Bronze plan to save $80 a month, then faces a $6,500 deductible after an unexpected ER visit. The math never worked in their favor, but the low premium felt safe.

In 2026, the return of the ACA subsidy cliff for higher incomes means that families earning just above certain thresholds could see their net premium spike dramatically. This is not a minor adjustment. It changes the entire calculus for households in the $60,000 to $100,000 income range.

The real differentiator is doing a thorough network and formulary check, not just a cost comparison. We have seen families save thousands simply by switching to a plan that covered their specialist in-network, a detail they nearly missed. Reviewing comparing smart picks by type gives you a framework to do this systematically. Expert guidance does not just save time, it often pays for itself in the first year.

Get expert guidance for your 2026 health insurance decision

You have learned the process. Now consider how professional support can make the final choice easier and more accurate for your specific situation.

At Strawderman Financial, our health insurance experts work directly with individuals and families to match the right plan to your real needs, not just your budget. We factor in your providers, your prescriptions, your income, and your timeline. If you are also planning for retirement and need to bridge the gap before Medicare, we help you build a strategy that protects your health and your finances at the same time. Schedule a free consultation and let us do the heavy lifting so you can enroll with confidence.

Frequently asked questions

How do I estimate my total yearly cost for health insurance?

Add your annual premium total to your expected out-of-pocket spending, including copays and coinsurance, then factor in your deductible and out-of-pocket maximum for worst-case planning.

Who qualifies for premium tax credits in 2026?

Individuals earning 100 to 400% of the federal poverty level generally qualify, and some above that threshold may still receive credits if premiums exceed a set percentage of income, based on 2026 eligibility thresholds.

Should early retirees get a different health insurance plan before Medicare?

Yes. Early retirees need a bridge plan that covers the gap until Medicare at 65, and 2026 premium and subsidy changes make careful income-based planning especially important during this period.

How can I check if my doctor or prescription is covered?

Use each plan’s online provider directory and drug formulary before enrolling. Checking network and formulary details before you sign up is the single most effective way to avoid surprise costs.

Recommended

Comments