How to compare insurance policies for retirement

- JF Strawderman

- 21 hours ago

- 9 min read

TL;DR:

Comparing insurance requires understanding your specific needs and evaluating coverage for life, health, and supplemental policies.

Organize key policy details like premiums, coverage limits, and insurer ratings side-by-side for accurate comparison.

Regularly review and compare policies annually to ensure coverage aligns with changing circumstances and long-term goals.

Staring at a stack of insurance policy documents, each with different premiums, exclusions, and benefit caps, is enough to make anyone freeze. For families and individuals trying to secure their financial future, choosing the wrong policy can mean gaps in coverage exactly when you need it most. The good news is that comparing insurance policies does not have to feel like solving a puzzle in the dark. With a clear process, you can identify which life, health, and supplemental insurance options truly fit your retirement goals, avoid costly mistakes, and make decisions you feel confident about for years to come.

Table of Contents

Key Takeaways

Point | Details |

Define your insurance goals | Clarifying your needs ensures you compare policies that truly protect your retirement plans. |

Organize and compare details | Collect all policy information—benefits, costs, exclusions—before weighing your options. |

Look past premiums | Consider company reputation and claims records, not just the lowest price. |

Avoid common mistakes | Don’t overlook pre-existing condition rules, waiting periods, or enrollment windows. |

Review yearly | Annual insurance check-ups help keep your retirement plan on track and fully protected. |

Know your insurance needs and goals

Before you compare a single policy, you need a clear picture of what you actually need. This sounds obvious, but most people skip this step and jump straight to pricing. That leads to buying coverage that looks affordable on paper but leaves real gaps when it matters.

Start by thinking about the three main types of insurance relevant to retirement:

Life insurance: Replaces income for dependents, covers debts, or funds a legacy for your family.

Health insurance: Covers medical expenses, hospital stays, prescriptions, and preventive care.

Supplemental insurance: Fills gaps left by primary coverage, such as critical illness, dental and vision, or burial insurance.

Each type serves a different purpose, and you may need more than one. The right mix depends on your family size, how close you are to retirement, and what coverage you already carry.

Next, estimate how much coverage you actually need. A good starting point is to calculate your monthly living expenses, any outstanding debts like a mortgage, and the income your family would lose if you passed away or became seriously ill. For retirement planning, factor in how long your savings need to last and whether Social Security will cover your basic needs.

Before you start comparing policies, gather this information:

Current insurance policies and their coverage limits

Your health history and any ongoing medical conditions

Monthly budget available for premiums

Retirement timeline and expected income sources

Family obligations and dependents

As the Medicare guide notes, you should assess needs based on family size, retirement horizon, and existing coverage before shopping for new policies.

Pro Tip: Write down your top three financial fears for retirement, whether that is a major illness, outliving your savings, or leaving debt behind. Let those fears guide which insurance types you prioritize.

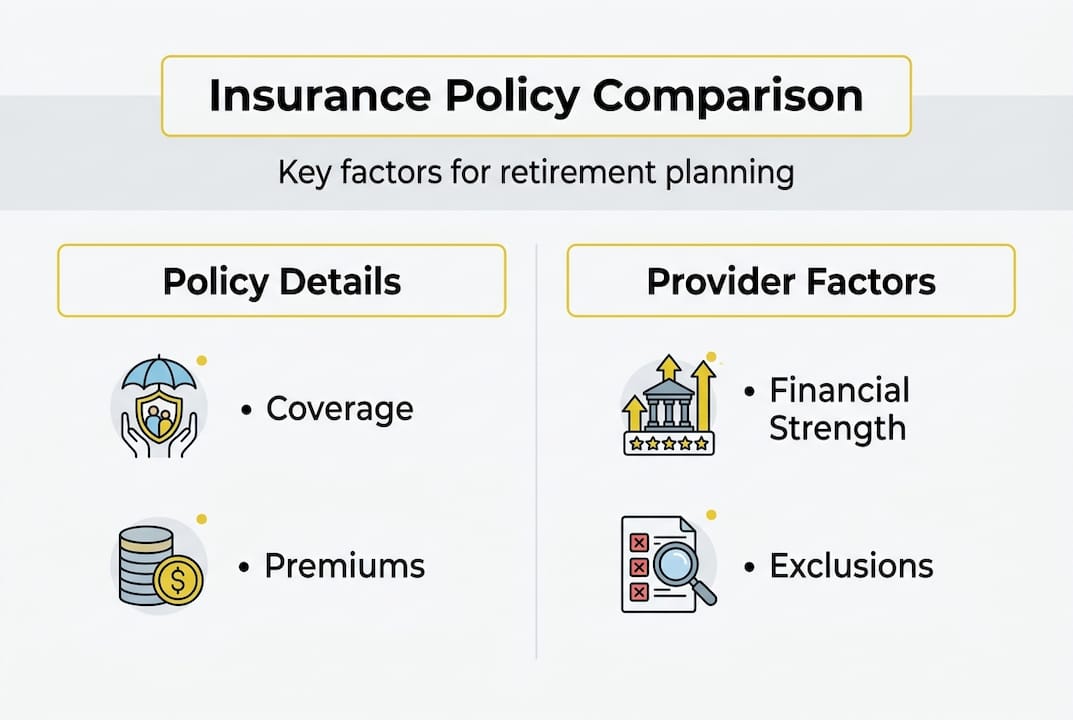

Gather key policy details for accurate comparison

Once you have a sense of your needs and goals, the next step is collecting key details from possible insurance policies. Without this information organized in one place, you are essentially comparing apples to oranges.

Here are the critical details to collect from every policy you consider:

Monthly premium: What you pay regardless of whether you use the coverage.

Coverage limits and benefit maximums: The most the policy will pay out.

Deductibles and co-pays: What you owe before the insurer pays and your share per visit or claim.

Exclusions: Conditions, treatments, or events the policy does not cover.

Waiting periods: How long before certain benefits become active.

Insurer financial strength rating: Scores from agencies like AM Best or Standard and Poor’s that show how likely the company is to pay claims.

Claims payout data: The percentage of claims the insurer actually pays.

Understanding policy terms matters. A waiting period means you cannot claim certain benefits right away after buying a policy. A benefit maximum is the ceiling on what the insurer will pay for a specific condition or over your lifetime. Knowing these definitions prevents nasty surprises.

Use a simple table to organize what you find. Here is an example:

Policy detail | Policy A | Policy B | Policy C |

Monthly premium | $180 | $240 | $210 |

Coverage limit | $250,000 | $500,000 | $350,000 |

Deductible | $1,500 | $800 | $1,200 |

Waiting period | 90 days | None | 60 days |

Insurer rating | A | A+ | A |

For life insurance comparison or reviewing health insurance options, this kind of side-by-side layout makes patterns obvious fast. As the Medicare resource confirms, critical factors include premiums, coverage amounts, exclusions, out-of-pocket costs, pre-existing conditions, and waiting periods.

Compare features, costs, and financial strength side-by-side

With all necessary details organized, it is time to directly compare what each policy offers. Numbers alone do not tell the full story, so you need to weigh costs against real-world value.

Here is a comparison framework across common policy types:

Feature | Whole life | Term life | Supplemental health |

Premium cost | Higher | Lower | Moderate |

Cash value | Yes | No | No |

Coverage duration | Lifetime | Fixed term | Renewable annually |

Typical exclusions | Few | Some | Condition-specific |

Best for | Legacy and savings | Income replacement | Gap coverage |

When comparing, pay close attention to:

Pre-existing conditions: Some policies exclude them entirely; others cover them after a waiting period.

Renewal options: Can the insurer raise your premium or cancel your policy at renewal?

Claim procedures: How easy is it to file a claim, and how quickly does the company pay?

Riders and add-ons: Optional features that expand coverage, such as a waiver of premium if you become disabled.

One of the most overlooked factors is insurer financial strength. A policy is only as good as the company behind it. Ratings from agencies like AM Best, Moody’s, and J.D. Power tell you whether a company has the financial muscle to pay claims years from now. The Medicare guide warns that you should avoid simply choosing the cheapest plan and instead check for strength ratings and examine claims data to ensure reliability.

For a broader view of how insurance fits into your long-term financial picture, exploring building wealth with insurance can help you see coverage as an asset, not just an expense.

Pro Tip: Use free online comparison tools like those offered by your state insurance department to cross-check premium quotes and insurer ratings before committing to any policy.

Common pitfalls and how to avoid them

Even with thorough comparisons, pitfalls can undermine your choices if you are not aware of them. Knowing what to watch for saves you from expensive regrets.

The most common mistakes people make when comparing insurance policies:

Chasing the lowest premium: A cheaper monthly payment often means higher out-of-pocket costs when you actually need care.

Ignoring exclusions: Skipping the fine print can leave you uninsured for the exact condition you were worried about.

Missing open enrollment windows: Buying outside open enrollment can mean higher costs or outright denial of coverage.

Not checking renewal terms: Some policies lock in low rates early but spike dramatically after age 65.

Overlooking the insurer’s claims history: A company with a poor claims payout record can deny or delay benefits when you need them most.

“Pre-existing condition exclusions and misleading premium structures are among the most common edge cases that catch policyholders off guard.” This is why reading every section of a policy document, not just the summary, is non-negotiable.

As the Medicare resource highlights, edge cases include pre-existing condition exclusions and misleading premium structures that can leave you underinsured.

Practical steps to protect yourself:

Read the exclusions section of every policy before signing.

Ask your agent specifically what is NOT covered.

Confirm renewal terms in writing.

Set a calendar reminder to review your policies every year and after any major life event such as marriage, a new child, or a health diagnosis.

For personalized guidance navigating these details, insurance agency support from a dedicated professional can make a real difference.

Checklist for final selection and annual review

To help you act on all you have learned, here is a practical checklist that covers both initial choice and annual review. Print it out or save it somewhere easy to find.

Before you choose a policy:

Confirm the policy covers your top three financial concerns.

Verify the insurer’s AM Best or J.D. Power rating is A or higher.

Calculate total annual cost including premiums, deductibles, and co-pays.

Read the exclusions section completely.

Confirm waiting periods and when full coverage begins.

Ask about renewal terms and whether premiums can increase.

Check that the policy aligns with your retirement review tips and long-term income plan.

At your annual review:

Compare your current policy against at least two alternatives.

Update your coverage if your health, income, or family situation has changed.

Check if your update life insurance needs have shifted due to a paid-off mortgage or a grown child.

Use Healthcare.gov to review health plan options during open enrollment.

Document all changes and keep copies of updated policies in a secure location.

The Medicare guide recommends that you shop annually and use government or reputable comparison tools to keep your coverage optimal as your needs evolve.

Pro Tip: Set a recurring annual calendar event titled “Insurance Review” every October, which aligns with open enrollment season for most health plans. Treat it like a financial checkup.

Why a methodical comparison beats shortcuts every time

Finally, it is worth considering the bigger lesson experienced financial planners stress about insurance selection. We have seen what happens when people rush this process. They pick a policy based on a friend’s recommendation or a flashy ad, and two years later they are fighting a denied claim for a condition buried in the exclusions.

Here is a perspective that surprises many people: a policy with a higher monthly premium can actually cost you less over a decade. If it has lower deductibles, fewer exclusions, and a stronger claims payout record, you keep more money in your pocket when it counts. Cheap coverage that fails you is not a bargain. It is a liability.

Small details compound over time. A 90-day waiting period on a supplemental policy sounds minor until you have a health event in month two. A renewal clause that lets the insurer raise your rate after 65 can double your costs right when your income drops.

The families who build lasting financial security through insurance and long-term wealth strategies are the ones who treat insurance comparison as a discipline, not a one-time task. They review annually, ask hard questions, and work with advisors who know the fine print.

Get expert guidance for your insurance comparison

Navigating life, health, and supplemental insurance options on your own is possible, but it takes time and expertise that most people simply do not have. Working with a knowledgeable advisor can help you cut through the noise and find coverage that genuinely fits your retirement plan.

At Strawderman Financial, our agents specialize in helping individuals and families across the U.S. compare expert life insurance help, health coverage guidance, and retirement planning services with no pressure and no guesswork. We offer free consultations so you can ask every question, understand your options, and make a confident decision. Your financial security in retirement is too important to leave to chance. Reach out today and let us help you build a coverage plan that works.

Frequently asked questions

What are the most important factors when comparing insurance policies?

Focus on premiums, coverage limits, exclusions, and insurer financial strength ratings, then match each factor to your specific retirement goals. As the Medicare guide confirms, key factors include premiums, coverage, exclusions, and insurer ratings.

How often should I compare or switch insurance policies for retirement?

Review your policies at least once a year and after any major life change such as a new diagnosis, marriage, or income shift. The Medicare resource advises that you shop annually and use comparison tools to ensure your coverage stays optimal.

How do pre-existing conditions affect my insurance comparison?

Pre-existing conditions can raise your premiums, trigger waiting periods, or limit certain benefits depending on the policy, so always read the fine print carefully. The Medicare guide notes that edge cases: pre-existing conditions waiting periods in health policies are among the most common surprises policyholders face.

Should I always go for the cheapest policy?

No. A low premium often comes with higher out-of-pocket costs, weaker coverage, or a poor claims record that can cost you far more in the long run. The Medicare resource is clear that you should avoid cheapest without strength ratings or claims data to back it up.

Recommended

Comments